Taxation

1. The original tax procedure

2. Types of taxes

- Corporate income tax is a direct tax on the income of an organization, a legal entity.

- Value-added tax is a tax imposed on the added value of goods or services arising in processing stages from production, circulation to consumption in Vietnam.

- Personal income tax is a direct tax imposed on the income of individuals living, working or doing business in the territory of Vietnam.

- Import and export tax are indirect taxes levied on goods exported or imported across the national borders.

- Foreign contractor tax is the adjusted tax for foreign organizations and individuals that do not operate under Vietnamese law and earn income from the providing services or services associated with goods in Vietnam.

- Special sales tax is a tax on certain goods and services on the list of State regulations on adjusting production or guiding consumption.

- Environmental protection tax is imposed on certain goods and products having detrimental influences to the environment as using.

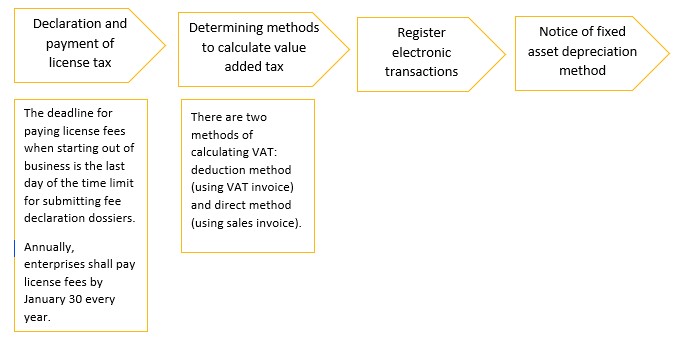

- License tax is a direct tax and is usually levied on the business license of the business and household businesses.

- Other tax such as natural resources tax, non- agricultural land use tax…

3. Submission timeline for tax declaration and reports applied for Foreign Invested Enterprise

Enterprises established in Vietnam must report to the functional agencies on their activities monthly, quarterly and year-end. As follows:

- Audited Financial Statements;

- Tax declaration and tax finalization for VAT, PIT, CIT….;

- Report of labor change;

- Report of the status of implementation of investment project.

4. Transfer pricing

There is transfer pricing regulation which outlines various situations where transactions among/ between related parties must be conducted on arm’s length basis. For compliance purpose, an annual declaration of related party transactions and transfer pricing methodologies used is required to be filed together with CIT return.

Vietnam’s tax authority follows a three-tier documentation approach and stipulated declaration forms which are required to be submitted in the last day of the 3rd month from the end of the calendar year or the fiscal year as regulated in the Decree 20/2017/NĐ-CP, Circular 41/2017/NĐ-CP and Law on Tax administration 38/2019/QH14. Vietnam’s tax authority stepping up its efforts in transfer pricing audit programs that target enterprises specifically with significant related party transactions, persistent losses or low - margins compared to other industry player.