Deals Dispatch - UK Technology

M&A update for Q1 2025

The UK technology sector has navigated another eventful period in Q1 2025. Sadly, there was little encouragement for the sector announced in the Spring Statement, despite continued sluggish growth in the wider UK economy. There were, however, further (if not new) references to investment in technology for the MoD and probation services and new digital skills for the civil service. Businesses have been bracing for the recent changes to National Insurance (effective 6 April), which will have had a significant impact on people-based tech companies. A reduction to Business Asset Disposal Relief has also now taken effect, but the impact on deal volumes is expected to be minimal.

Looking at the global picture, adverse US economic data and speculation around US tariffs resulted in the NASDAQ closing 13% down at the end of the quarter from its peak in February 2024. While the UK technology sector will not be immune to global uncertainty, the UK remains the leading tech ecosystem in Europe, contributing £150 billion Gross Value Added (GVA) to the UK economy each year while growing faster than any other sector.

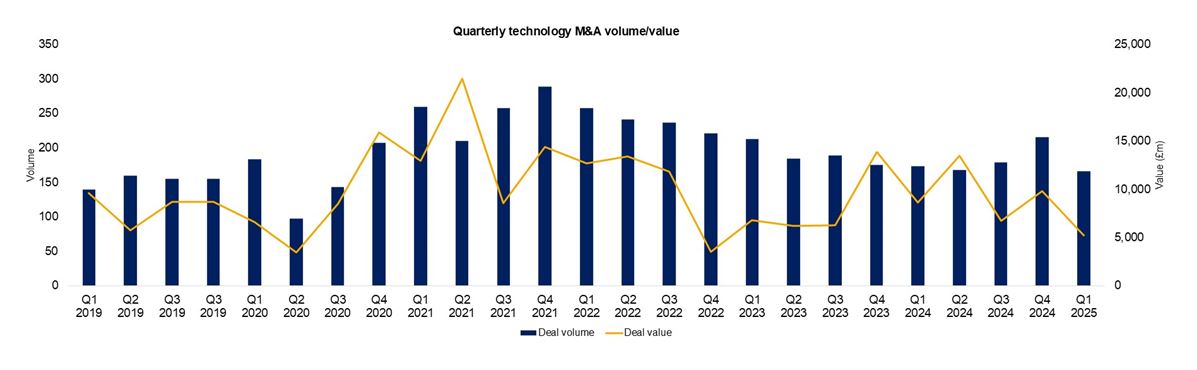

Unsurprisingly, deal volumes were 25% lower in the quarter, which was expected after the Budget-induced spike we saw in the previous quarter. Year-on-year deal volumes were also down 7%. Deal values were more significantly impacted; 47% down on the quarter and 39% down on the year, largely due to a lower number of high value (>£250 million) transactions.

Deal volumes seem to have settled at a level above where they were in 2019. Software companies have led the charge, with typical characteristics including recurring revenues and predictable cash flows underpinning investment confidence in an unstable economic environment. We expect this trend to continue in the short term.

Domestic stagflation is being compounded by international trade wars between the world’s largest economies. The Bank of England has urged not to presume a preset path of rate reductions, given the current environment. This uncertainty remains a blocker for the UK technology M&A market, and we are unlikely to see significant growth in transaction volumes until it resolves.

However, growing demand for new technologies and related services has meant the sector has proven itself to be resilient. Embedding technology into business strategy and operations is essential for driving growth, productivity and cost saving. As we enter the era of AI, it is crucial for companies across all sectors to continue investing in technology (selectively) to avoid being left behind. This bodes well for the UK technology sector. With CGT rate changes remaining minimal (for now), we expect owner-managers with exit ambitions to be considering their options. The buyer/seller value expectation gap that existed following the decline in pricing from the peak of 2022 has now also tightened, which should also help the momentum of transactions. Overall, we maintain a positive but cautious outlook for the rest of the year.

Deal dispatch Q2 2025

Deal dispatch Q4 2024

Deal dispatch Q3 2024

Deal dispatch Q2 2024

Deal dispatch Q1 2024

Deal dispatch Q2 2025

Deal dispatch Q4 2024

Deal dispatch Q3 2024

Deal dispatch Q2 2024

Deal dispatch Q1 2024