The UK building services sector is generating more investor interest, more transaction activity, and more capital deployment than at any point in the past decade.

For businesses operating in HVAC maintenance, mechanical and electrical services, planned preventative maintenance, lift servicing, water hygiene, energy management, and related hard Facilities Management (hard FM) disciplines, the fundamentals have never been stronger and the demand for what they have built has never been greater.

The Market in 2026: Structural tailwinds across the sector

Compliance has become a permanent growth driver

The compliance obligations placed on building owners, managing agents, and responsible persons have expanded significantly in recent years and show no sign of abating. Successive waves of building safety and energy efficiency legislation, covering everything from fire safety certification and water hygiene management to energy performance standards and mechanical system inspection, have increased the volume and frequency of mandated work across the built environment.

The critical point for building services businesses is that this demand is non-discretionary. Customers cannot cancel a planned maintenance schedule without exposing themselves to regulatory and legal risk. Annual service agreements, statutory inspection cycles, and compliance certification programmes create a recurring revenue base that is structurally insulated from economic cycles in a way that project-based businesses simply cannot replicate.

Across HVAC, Mechanical and Electrical (M&E), water hygiene, lift servicing, and related disciplines, the legislative backdrop is consistently pushing compliance requirements upward, expanding the addressable market for qualified, accredited providers while simultaneously raising the barrier to entry for new competitors.

Hard FM has become the dominant investment theme

The facilities management sector has experienced a decade of sustained M&A activity, with more than 1,750 transactions completing in the past 12 years. Within that overall volume, the composition has shifted decisively. Hard and technical services, the businesses with contracted, recurring, compliance-driven revenue, now account for over half of all FM deal activity. This is not cyclical noise. It is a structural reallocation of capital toward the most resilient, most defensible end of the market.

Building maintenance and M&E transaction activity accelerated in 2025 relative to 2024, with fire and life safety sub sectors seeing a clear uplift in deal volumes. Increased activity has also been evident across lift servicing, water hygiene and energy management, as buyers target businesses with the same underlying characteristics that have long made fire safety attractive: recurring revenues, defensible customer relationships and demand supported by regulation.

Deal volumes have reached record levels

2025 was a record year for UK FM and building services M&A. After some caution earlier in the year as the market absorbed the impact of employer National Insurance Contribution (NIC) increases and waited for clarity on interest rates, Q4 delivered its strongest quarter on record. With private credit markets increasingly competitive and the Bank of England base rate on a downward trajectory, the debt conditions supporting deal activity have materially improved from the peak-rate environment of 2023.

The pipeline for 2026 remains strong. A backlog of ownership transitions deferred through the uncertainty of 2024 to 2025 is now moving. The rising rate of Business Asset Disposal Relief, which reached 18% in April 2026, has accelerated the decision-making of long-standing owner-managers. Combined with an active pool of PE-backed consolidators hungry for bolt-on targets, the conditions for continued high deal volumes are firmly in place.

Why recurring revenue changes the valuation conversation

The most important distinction in building services M&A is not between sub-sectors. It is between revenue models. A business with £5 million of contracted maintenance revenue is a fundamentally different proposition to a £5 million project business, regardless of whether it operates in HVAC, M&E, lifts, or water treatment.

| Contracted, recurring income provides the forward cashflow visibility that underpins confident deal structuring for both acquirers and lenders. It reduces earnings volatility, supports higher EBITDA multiples, and makes the business significantly easier to finance. |

For acquirers and investors, the recurring revenue base delivers three things that project revenue cannot: forward visibility of cashflow before a deal completes; a revenue floor that reduces downside risk in underwriting; and a platform for growth, because every maintenance contract is also a relationship that can be extended, cross-sold, and retained through a change of ownership.

High renewal rates compound the advantage. Building services customers, particularly those in regulated sectors such as social housing, NHS estates, and commercial real estate, face real reputational and legal risk from switching to an unknown provider. The practical consequence is retention rates that consistently outperform most other service sectors, and contracted revenue today that is a strong proxy for contracted revenue next year.

The valuation evidence is unambiguous. Mid-market building services businesses with strong recurring revenue profiles are transacting at 4.5x to 6.0x EBITDA, with material premiums reaching 7.5x and above for businesses that combine high contract renewal rates with self-delivery capability and a diversified customer base. The multiple compression seen in some other sectors through 2023 to 2024 has been notably absent here.

The deal market: Who is buying and why

A fragmented market still rich with opportunity

Despite sustained M&A activity, the UK building services sector remains highly fragmented. The majority of businesses across HVAC, M&E, planned maintenance, lifts, and water treatment are still owner-managed, sub-scale regionally, and operating without institutional backing. This fragmentation is precisely what makes the sector compelling to buyers: the consolidation opportunity is far from exhausted.

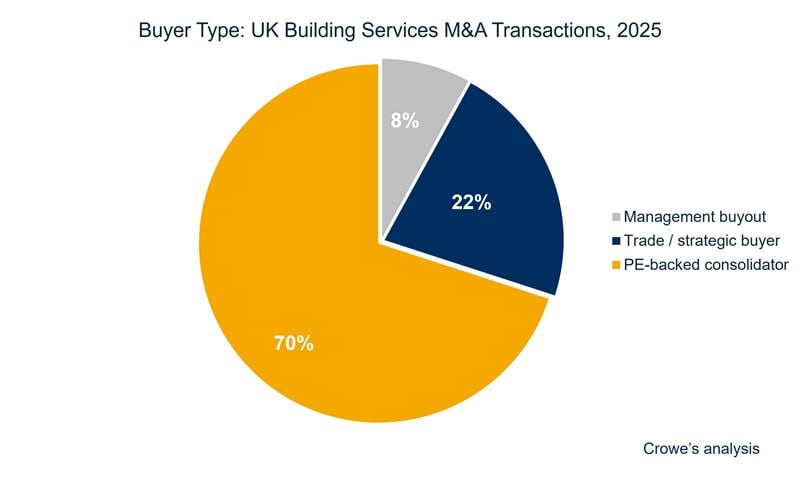

The buyer landscape

Three distinct buyer types are active in the market, each with different motivations and deal structures.

- PE-backed consolidators: PE-backed consolidators are the dominant force, driving the majority of transactions. These platforms are well-capitalised, acquisition-experienced, and actively seeking regional owner-managed businesses that add geography, engineering headcount, or customer relationships to an existing platform. They move quickly and bring competitive tension to any process.

- Trade and strategic buyers: Trade and strategic buyers are expanding capability and market reach, often acquiring specialist businesses in adjacent sub-sectors to broaden service offerings. Cross-selling potential and geographic expansion are the primary strategic rationale.

- Management buyouts: Management buyouts remain a consistent route for ownership transition, particularly where the founding owner wants to ensure continuity for staff and customers and the incumbent management team has the operational capability to run the business independently.

The breadth and depth of buyer appetite in this sector is not matched in many parts of the mid-market. For businesses of the right quality, competitive processes are generating multiple offers and that competition is sustaining valuations even as deal activity accelerates.

What drives value: The four factors that separate good outcomes from great ones

Understanding what buyers are actually looking for, beyond the headline financials, is the most important thing an owner-manager can do before entering any transaction process. The businesses commanding premium outcomes share four consistent characteristics:

Beyond these four, there are structural factors that increasingly influence buyer appetite: the presence of a management team that does not depend entirely on the founder; documented systems and processes that survive a transition; a forward order book that demonstrates a pipeline; and a technology or data capability that supports service delivery and positions the business for the next phase of the market's evolution.

How Crowe works in this sector

Crowe's Corporate Finance team has extensive experience advising owner-managed building services and hard FM businesses across the full transaction cycle.

We understand the sector: the revenue model, the customer dynamics, the accreditation landscape, and the deal structures that work at this end of the market.

We work with business owners who are thinking about a sale, at any stage, helping them understand current market value, identify what would maximise that value, and run a process that generates competitive tension among credible buyers. We work with businesses looking to acquire, providing target identification, commercial and financial due diligence, deal structuring, and funding support. And we work with management teams exploring buyout options, structuring transactions that work for both the exiting owner and the incoming leadership.

In every case, the starting point is the same: a direct, honest conversation about where the business sits in the current market and what the realistic options look like. There is no obligation, and there is no cost to that initial discussion.

Confidential, no-obligation conversation. We'll give you an honest view of where your business sits in this market.

DisclaimerThis document is produced by Crowe U.K. LLP for general informational purposes and does not constitute financial advice or a formal offer of services. Market statistics are drawn from publicly available sector deal data and industry research. Sub-sector activity figures and EBITDA multiple ranges are indicative. |

Contact us