The Testing, Inspection and Certification (TIC) sector remains one of the most attractive areas of the UK Business-to-Business (B2B) services market. Offering a compelling combination of non-discretionary demand, recurring revenues, regulatory-driven growth, market fragmentation and multiple routes to value creation, the sector continues to demonstrate many of the characteristics that investors value in uncertain markets.

M&A momentum remains robust despite broader market caution, with more than 280 UK TIC transactions recorded by Crowe UK in 2025 and Q1 2026 activity ahead of the prior year. While valuations remain nuanced, high-quality TIC assets continue to command attractive multiples, reinforcing the importance of early preparation for shareholders considering an exit.

The UK TIC sector: Structurally attractive and still fragmented

With the UK economy moving into a more stable phase, inflation at 2.8% in the 12 months to May 2026 and the Bank of England’s base rate held at 3.75%, there are early signs of improving confidence in M&A activity, though buyers remain selective and diligence is more rigorous.

The UK TIC market continues to expand across a range of areas such as renewable energy technologies, environmental testing, food testing, fire safety and air and water quality testing. This broader service evolution is important: buyers are increasingly looking for specialist platforms that can support customers through multiple compliance, safety and sustainability challenges.

The key attractions for investors are clear.

- Regulatory demand: Many services are legally required or embedded in customer risk frameworks.

- Recurring revenue: Periodic inspections, audits, certifications and testing cycles support visibility.

- Mission-critical service delivery: Customers may be reluctant to switch provider where accreditations, technical knowledge and compliance records are important.

- Fragmentation: Many TIC niches remain populated by founder-owned, specialist SMEs.

- Scope for consolidation: Private equity-backed and strategic platforms can create value through buy-and-build, systems investment, cross-selling and professionalisation.

- Global credibility: As a global leader in regulatory standards, UK TIC businesses often benefit from internationally recognised technical expertise and accreditations.

M&A momentum: Consolidation is accelerating

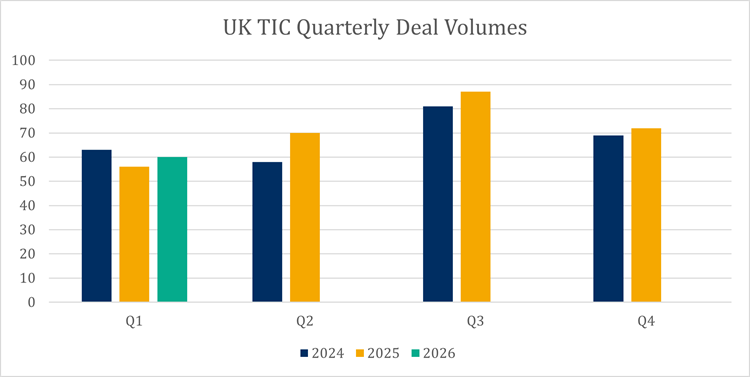

UK TIC deal activity, tracked by Crowe UK, has remained remarkably consistent despite a period of wider M&A volatility driven by inflation, higher interest rates and more cautious lending markets.

More than 280 announced transactions were recorded in 2025, up from 270 in 2024, demonstrating the resilience of buyer appetite for compliance-led and safety services. This momentum has continued into 2026, with 66 transactions identified in Q1, ahead of the 56 recorded in Q1 2025, reinforcing the view that TIC remains one of the more attractive areas of the broader B2B services market for investors.

Sources: MarktoMarket, Beauhurst, Pitchbook, Crowe UK analysis

The sector continues to show repeated activity from a group of well-known consolidators, including Phenna Group, Wilmington plc, Celnor Group and SGS. Their activity supports the view that TIC M&A is not simply a series of one-off strategic acquisitions; it is an increasingly structured consolidation market with many smaller consolidators, such as Ranger Fire & Security, following suit.

In the UK, private equity-backed platforms are particularly active. Phenna Group, backed by Oakley Capital, acquired 25 businesses in 2025 alone, while Celnor Group, backed by Inflexion, has acquired more than 40 businesses across environmental consultancy, surveying, ecology, geotechnical services and specialist inspections since 2023.

For owner-managers, this represents a broad potential buyer universe. A specialist lower-mid market TIC business may appeal not only to direct trade buyers, but also to private equity-backed platforms seeking capability expansion, regional density, or broader end-user market exposure.

Crowe UK has seen this first-hand through its recent activity in the sector, including advising on transactions involving i2 Analytical, IFC Group, Altitec Blade Services, BASEC Group, together with health and safety training providers Astutis and Phoenix Health & Safety.

Recent sector deals point to sustained appetite

Recent key transactions demonstrate the breadth of buyer appetite across TIC and a willingness to invest heavily into the sector’s future.

- EQT / Intertek – June 2026 - Intertek agreed a takeover by EQT valuing the business at approximately £10.9 billion including debt, with the offer representing a 40% premium to Intertek’s closing price before the first approach was made public.

- Inflexion / Ranger Fire & Security - June 26 - Inflexion acquired a majority stake in Ranger Fire & Security alongside a reinvestment by existing investor, Hyperion Equity Partners. The transaction highlights continued private equity appetite for compliance-led fire and security services and validates Ranger’s rapid expansion strategy.

- Axis CLC Group / Fieldway Group – June 2026 - H.I.G. Capital-backed Axis CLC Group acquired Fieldway Group, a UK fire safety and compliance specialist serving the social housing sector, from Foresight Group. The acquisition expands Axis CLC’s presence in North West England and supports its strategy of building a leading national compliance and maintenance platform.

The message is consistent: scale platforms are willing to pay premium multiples for assets with specialised capability, defensible margins, recurring revenue and exposure to structural growth themes such as energy transition, digital compliance, product safety and regulated infrastructure. We highlight the key drivers to value below.

Valuation multiples: Stable overall, premium for quality

TIC valuations continue to outperform many B2B services sectors, with listed peers typically trading at 10x–13x EV/EBITDA despite a more cautious M&A market. The strong performance of scaled platforms such as Intertek and SGS highlights continued investor appetite for businesses offering recurring revenues and regulatory exposure.

Crowe UK’s tracked transactions, where multiples are disclosed, show a general range of 7.5x-12.5x with higher multiples saved for premium assets with specialist technical expertise and recurring compliance-led revenues with defensible market positions. A recent example being the reported c.10x multiple paid by Certania for ICA Group, a quality testing and compliance consultancy business in the construction space.

For sellers, the direction of travel is therefore not simply “multiples are up” or “multiples are down”. The market is more nuanced. Larger, specialist, well-invested TIC businesses with attractive growth, strong margins and defensible accreditations can command premium valuations. Smaller businesses with customer concentration, limited management depth, low investment in systems or weaker growth may still transact, but buyers will price this risk more carefully.

What does the future hold for the TIC sector?

The outlook for the TIC sector remains positive, with long-term growth expected to be driven by structural rather than purely economic factors. Regulation is becoming broader and more complex across areas such as building safety, fire safety, product conformity, environmental standards, workplace safety, utilities, infrastructure and energy transition. Recent examples being the Fire Safety (Residential Evacuation Plans) (England) Regulations 2025 and mandatory digital waste tracking scheduled to apply from October 2026. This is bolstered by continued infrastructure spending, such as AMP8, which will require compliance services.

At the same time, customers are increasingly outsourcing compliance and assurance activities, creating continued demand for accredited providers with specialist technical expertise, recurring service models and strong regulatory credentials.

Looking ahead, the sector is likely to be shaped by energy transition, sustainability, digitalisation and consolidation. Renewables, grid infrastructure and offshore wind are expected to create significant new demand for independent verification, testing and assurance. Technology will also play a larger role, with digital scheduling, customer portals, remote monitoring, drones, sensors and AI-assisted inspection improving efficiency and customer value.

Key value drivers

For shareholders considering a sale, value is driven by more than EBITDA. Buyers will focus on the quality, resilience and scalability of earnings. The most important value drivers we have seen across TIC-related deals typically include:

- Recurring and compliance-led revenue: Businesses with recurring inspection, testing, certification or compliance revenues are generally more attractive than those reliant on project-based income.

- Accreditation, technical capability and reputation: Strong accreditations, specialist expertise and recognised technical credentials can create meaningful barriers to entry and support premium valuations.

- Organic growth and pricing power: Buyers favour businesses that can demonstrate sustainable organic growth, cross-selling opportunities and the ability to pass through cost inflation.

- Margin quality and cash conversion: Strong margins, efficient operations and reliable cash generation provide confidence in future performance and investment potential.

- Customer diversification: A diverse customer base, long-standing relationships and low customer concentration help reduce revenue risk.

- Management depth and succession: A capable management team beyond the founder provides buyers with confidence that the business can continue to grow post-transaction.

- Systems, data and digital capability: Robust systems, data management and digital processes can improve efficiency, scalability and customer retention.

- Exposure to growth themes: Businesses operating in areas such as energy transition, environmental compliance, fire safety, regulated infrastructure and product assurance continue to attract particularly strong buyer interest.

How Crowe UK can help

Crowe UK's Corporate Finance team offers deep experience in advising business owners, management teams, corporates and investors across TIC and related compliance-led sectors. For shareholders considering an exit, early preparation can make a significant difference to valuation, deal certainty and outcome.

We work with business owners who are thinking about a sale, at any stage, helping them understand current market value, identify how to maximise that value, and run a process that generates competitive tension among credible buyers. We work with businesses looking to acquire, providing target identification, commercial and financial due diligence, deal structuring, and funding support. And we work with management teams exploring buyout options, structuring transactions that work for both exiting shareholders, management and investors.

In every case, the starting point is the same: a direct, honest conversation about where the business sits in the current market and what the realistic options look like.

Contact us