The importance of Net Zero for Insurers

Insurance firms play a key role in the transition to Net Zero, and therefore require to have plans in place to support and promote a low-carbon economy.

The term Net Zero refers to achieving a balance between the amount of greenhouse gas emissions emitted in the atmosphere, and the amount removed from it over a specific period. This is crucial to limit global warming to 1.5°C above pre-industrial levels and avoid the most catastrophic impacts of climate change.

Based on an analysis performed by Greenpeace and WWF in 2021, the financial sector in the UK is ranked among the top 10 for carbon emissions. Considering the key role played by financial institutions, it is no surprise to see increasing external pressure on insurance firms to set transition-related objectives– in addition to the decarbonisation activities. Organisations are also expected to effectively manage climate-related risks and opportunities, and to contribute to the economy-wide transition through their products and services.

A growing number of insurance firms are considering how they address climate change as a key component of their business strategy, in particular, to align their business plans and activities with a Net Zero pathway. They are engaging with their key stakeholders, including shareholders, customers, employees and regulators, improving their understanding of climate risks and opportunities, and setting stretching yet achievable emissions reduction targets.

Getting the house in order

Insurance organisations that are looking to start their journey to Net Zero should first focus on having their house in order – identifying and managing their direct and indirect emissions linked to their operations is one of the key steps to be taken. While Scope 1 and Scope 2 emissions will be more easily analysed and managed, Scope 3 emissions will be likely to represent the highest component in the insurers’ emissions inventories.

Scope 3 emissions can be challenging, not only from a data availability and accuracy perspective but also in terms of emission reductions. When looking at the operational perspective, external parties - including vendors, suppliers and outsourcing partners - represent a key component of this scope, and the identification and management of their emissions can involve a long and complex process. Organisations will be required to effectively collect information around these indirect emissions and review their procurement process to enhance its sustainability focus – this should include the implementation of policies, enhanced due diligence and appropriate engagement plans.

Scope 3 also includes emissions related to the organisation’s investments and underwriting activities – these components will be covered in the sections below.

When looking at their operations, insurance firms should also consider how climate will be integrated into their existing risk management framework, including the analysis of their operational exposure to physical risks (e.g. flooding, wildfire, windstorm).

Recognising the impact of funded emissions

One of the most powerful influences that insurance firms have over the ‘real economy’ is how they chose to invest their asset portfolios. This can be an effective lever to support the transition to Net Zero through their ability to allocate capital.

While supporting ‘green’ portfolios is particularly important, insurance firms are also expected to use their funds to support the transition – this entails an appropriate engagement process where investees will be required to provide evidence of their climate-related performance.

a) ‘Green’ assets – debt or equity issued by organisations that have clear climate-related commitments and have integrated Net Zero considerations into their core business. These companies will be able to provide regular reporting on their performance and their short-term and long-term objectives and demonstrate a clear alignment of interest with insurers’ Net Zero pathways.

b) Transitioning organisations – these firms are in the process of setting targets and developing transition plans. While no major progress might have been achieved, they have clear plans in place to undertake their Net Zero journey. Insurance firms that are seeking to influence the ‘real economy’ have a key role to play in working with these types of organisations. They should monitor their progress closely, ensuring that capital support is provided to those companies who continue to provide evidence of their future transition.

c) ‘Brown’ assets – firms in this category may have no specific intention of integrating climate considerations into their business in the short term. Insurers may be tempted to divest these types of assets, but certainly, institutional investors have significant leverage through their investment stewardship to pressurise the boards and management of these organisations, perhaps in combination with other investors. These types of assets are significantly exposed to transition risk and result in ‘stranded assets’ for the insurance company, in the event of unexpected government or regulatory intervention. There may indeed come a point where both sides need to recognise that an alignment of interests is not possible.

Managing the implications of insured emissions

Underwriting is the core product of an insurance organisation and for any Net Zero programme to be credible, insurers need to make progress in addressing the impact of the organisations they chose to insure. While everyone recognises that doing this effectively represents a long journey, implementing the appropriate measures into the current underwriting processes will ensure insurance firms align their portfolio with the transition.

In the same way as with investments, insurers need to think in terms of allocating a gradually diminishing carbon budget to their underwriting activities, just as through Solvency II regulations they have grown used to capital allocation as a discipline. The carbon intensity of the underwriting portfolio is only one of a number of ESG metrics that organisations will be using to review their portfolio. Consideration will also need to be given to exposure to climate risk through transition and liability aspects.

Underwriting strategy will dictate areas where the business wishes to focus, for example developing solutions to the emerging clean energy sectors which are expected to thrive as a result of the transition. Inevitably in managing corporate reputations, there will be requirements to consider sectors and risk types which will be excluded from future underwriting activities, such as thermal coal, oil sands or arctic drills. Beyond that, each insurer will be continuing to actively refine their risk appetite and ensure their pricing and risk selection are appropriately set based on climate considerations.

When it comes to calculating the carbon intensity of its underwriting portfolio, the PCAF guidance published in November 2022, is particularly helpful in determining the current baseline footprint. Although this currently only applies to commercial and motor insurance, one can imagine the boundaries of this analysis will gradually expand to encompass all aspects of insurance. Despite the PCAF calculation having provided a very transparent and simple methodology, there will at least initially be a heavy reliance on estimates and proxy data given the limited availability of carbon emission data for non-listed companies.

In much the same way as described for investments, insurers will be driven by their Net Zero commitments to establish a carbon budget and allocate capital to different lines of business within their portfolio, naturally driving underwriters to dig deeper into how credible individual insured’s transition plans prove to be over time. The majority of insurers will seek to work with their clients to align themselves to their transition plans, whilst increasingly applying pressure to ‘brown industries’ less willing to engage.

Having said that, when it comes to underwriting, carbon intensity remains only one measure of a portfolio’s ESG performance and insurers will be required to understand their overall portfolio exposures to climate risks, including physical, transition and litigation risks. Even in this case, the use of climate scenario modelling is crucial to determine how these risk exposures are anticipated to develop over time and manage it accordingly.

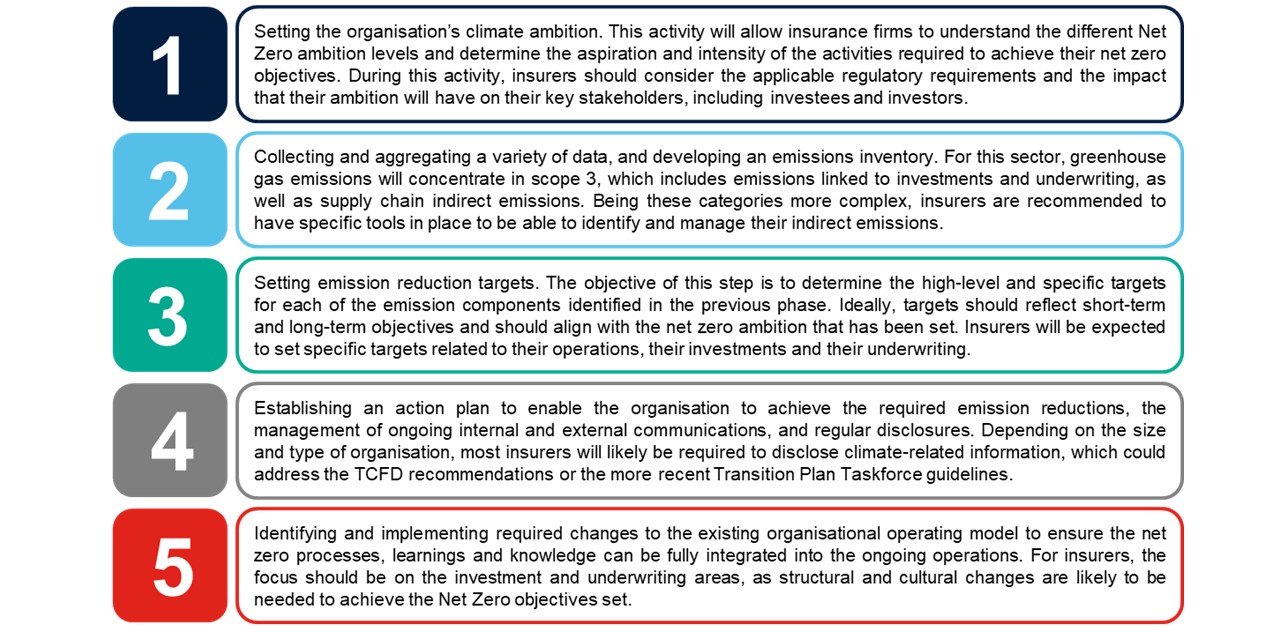

How to reach Net Zero

An increasing number of insurers are planning on taking action to achieve a more sustainable business. For a successful transition to Net Zero, organisations are working on a series of activities that can be summarised in the following building blocks.

How Crowe can help

In the current context, where keeping pace with the climate transformation is becoming increasingly difficult and requires complex choices, Crowe helps insurance firms to translate climate issues into opportunities, enabling them to determine the best approach and plan to address their climate ambition and add value to their business. Through our practical and experienced team, Crowe can offer different services, spacing from working with our clients to deliver an end-to-end solution to providing support by reviewing their work in specific areas. Please get in touch with Simona Villa or Alex Hindson or your usual Crowe contact for more information.