Deals Dispatch - UK Technology

M&A update for Q1 2026

It has been a quarter of considerable contrast, with early momentum based on a recovering deal environment and improving macroeconomic conditions making way for renewed uncertainty due to conflict in the Middle East, which is likely to shape the outlook for the remainder of 2026.

Against that backdrop, the UK technology M&A market has so far demonstrated resilience. Deal volumes held broadly in line with Q1 2025, and quality assets continued to attract strong interest, despite a recalibration of value expectations in response to both the macro environment and the structural questions raised by AI.

This edition explores those themes in detail, including an examination of the so called SaaSpocalypse, the sharp repricing of global software stocks that dominated headlines through February and March, and what it means for technology business owners in the UK mid market.

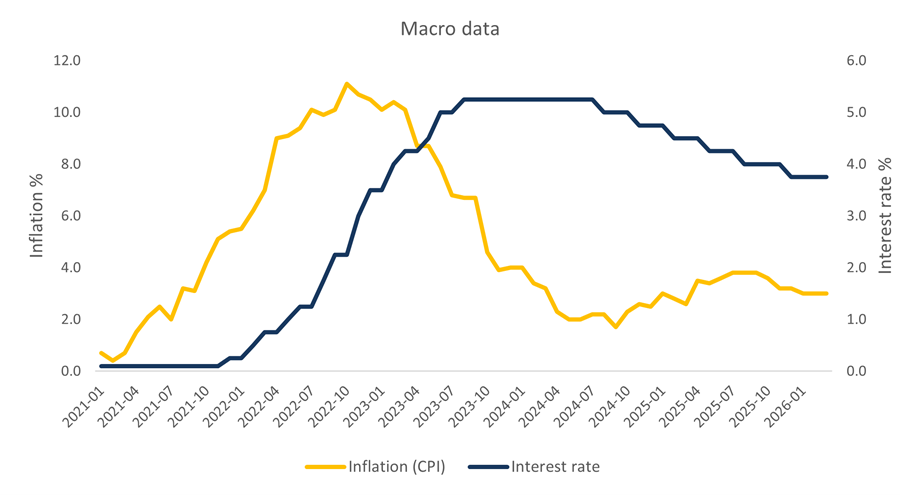

Entering 2026, the macroeconomic backdrop for UK M&A was more constructive than it had been at any point since 2022. Inflation was trending towards target, as a result interest rates were on a clear downward path (there were four 0.25% base rate cuts during 2025) and GDP growth, while fragile, was showing signs of genuine improvement.

The February 2026 GDP figures, released this month, reinforced that picture. The economy expanded by 0.5% month on month, the fastest pace since January 2024 and well ahead of the 0.1% consensus forecast. For technology M&A, this suggested a more supportive deal environment, with lower borrowing costs, improving confidence and a pipeline of businesses that had weathered a period of economic headwinds.

Conflict and uncertainty in the Middle East have since disrupted supply chains and materially altered the picture. The inflationary impact of higher oil prices is significant, with the Bank of England now expecting CPI to climb to 3.5% over the next six months and the IMF pencilling in a peak of 4%. As a result, interest rates are likely to be held until there is greater clarity. The IMF has also stated that the UK faces the biggest impact on growth from the conflict of any major economy, reflecting the country’s heavy reliance on imported energy.

The read for technology M&A is that the February GDP figures, encouraging as they were, are now backward looking. The environment for Q2 and beyond will be shaped by how quickly energy markets stabilise and whether a sustainable diplomatic resolution emerges. In the meantime, deal processes are facing more complex financing conditions than were anticipated at the start of the year, and business confidence, a key driver of investment decisions, has weakened. We do not expect these headwinds to derail activity materially, but in the short term vendors should plan for a return to greater scrutiny on earnings, longer deal timelines and deal structures that reflect any perceived additional risk.

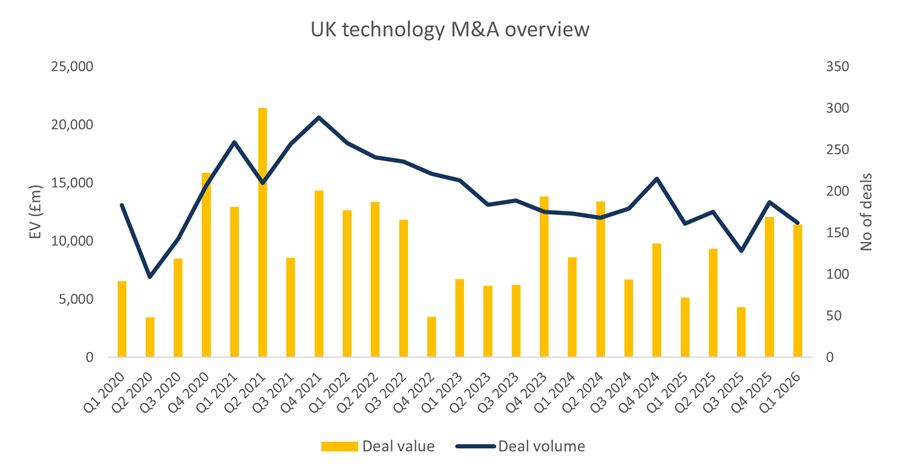

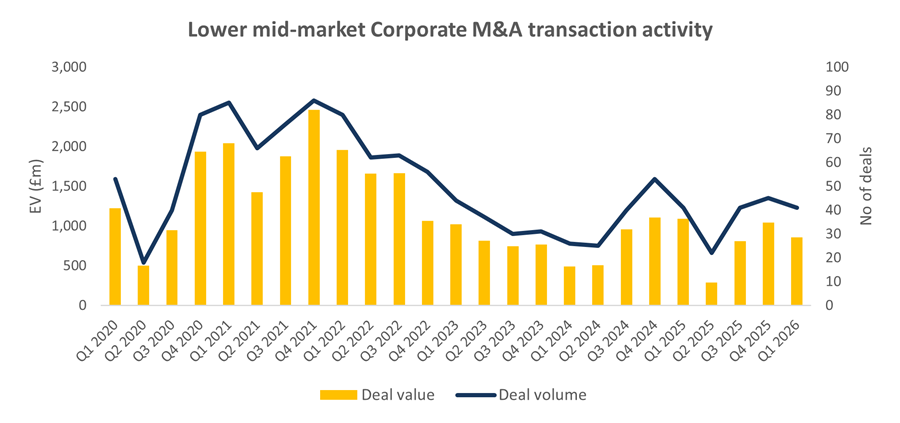

Turning to the deal data, Q1 2026 recorded 162 transactions in the UK technology sector, down 13% on the strong Q4 2025 we reported on in February. Activity in the quarter was broadly flat year on year against Q1 2025. This broadly supports the momentum we perceived coming into 2026. Total disclosed (and estimated) deal values of £11.4 billion were 5% lower than the prior quarter, but more than double Q1 2025 levels of £5.1 billion. This reflects, in part, the Virgin Media O2/Netomnia deal and the TPG investment in EMIS Group but also suggests a general shift towards higher value transactions as buyers concentrate capital on proven assets. Average deal sizes have risen accordingly, as the flight to quality dynamic has persisted, and vendors with strong recurring revenue profiles, defensible market positions and credible AI narratives continue to attract strong interest.

Looking ahead, we expect UK technology M&A activity to remain resilient through the remainder of 2026, notwithstanding any further macroeconomic shocks and with the expectation that global energy prices stabilise in the short term. Recent market uncertainty has not undermined the strategic rationale for transactions in the sector. Capital remains available and both financial sponsors and corporates continue to prioritise investment in technology enabled growth and efficiency.

Encouragingly, succession planning, converging technologies and the desire to supplement or accelerate organic growth continue to bring quality businesses to market. While buyers are being selective, with increased diligence and pricing discipline, they are willing to look at strategic opportunities. We therefore expect M&A activity to continue in line with and potentially ahead of 2025 levels.

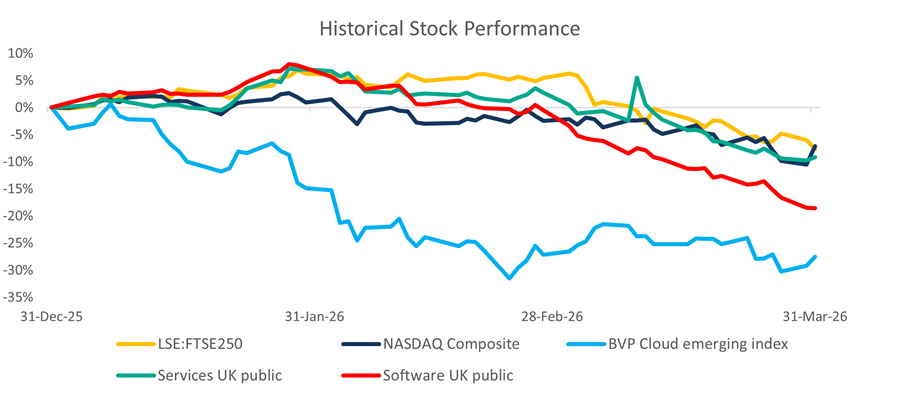

Public software markets were sharply unsettled in Q1 following the release of autonomous AI agents from OpenAI and Anthropic, which demonstrated the ability to execute complex business workflows with limited human intervention. These tools can also be embedded with little to no development skills. While software valuations were already under pressure entering the year (due to macro uncertainty, stretched US multiples and growing AI scepticism as previously reported), the announcement acted as a catalyst for a rapid sell off. EV to revenue multiples compressed materially across both US and UK listed software cohorts, and by mid-February average valuations had fallen 40-60% below recent three-year averages, briefly trading at discounts to the wider market.

While markets now broadly accept that the reaction was overdone, it has sharpened the split between simple, interchangeable software and platforms that are deeply embedded in customer workflows. Businesses that do not engage credibly with AI, particularly those reliant on per seat pricing, are now seen as higher risk. Larger players are expected to adapt over time, but the re-pricing underlines that this transition is not optional. For UK mid market technology businesses, public markets provide a clear signal. Adopting AI may create short term cost or margin pressure, but it is increasingly essential to defend relevance, support growth, and protect longer term value.

Sources: Pitchbook, Megabuyte, ONS, Bank of England, Financial Times, International Monetary Fund.

Deal Dispatch Q4 2025

Deal Dispatch Q3 2025

Deal dispatch Q2 2025

Deal dispatch Q1 2025

Deal dispatch Q4 2024

Deal dispatch Q3 2024

Deal dispatch Q2 2024

Deal dispatch Q1 2024

Deal Dispatch Q4 2025

Deal Dispatch Q3 2025

Deal dispatch Q2 2025

Deal dispatch Q1 2025

Deal dispatch Q4 2024

Deal dispatch Q3 2024

Deal dispatch Q2 2024

Deal dispatch Q1 2024