Transition Plan Taskforce deliver disclosure framework for climate transition plans

On Monday 9 October, Transition Plan Taskforce (TPT) launched the final Disclosure Framework for climate plans. Although the framework remains largely consistent with the previous version, clarity has been provided around the disclosure of specific elements and sub-elements. TPT is also expected to publish sector-specific guidelines for consultation in November, with the objective of finalising them in early 2024.

Organisations are now urged to initiate or progress their transition plan journey, ensuring their alignment with the framework.

The launch of the TPT Framework is particularly important within the financial sector, given the Financial Conduct Authority (FCA) has been involved in its development and strongly supports its adaptation. After its launch, the FCA communicated its commitment to draw on the TPT Framework – as well as the International Sustainability Standards Board (ISSB) standards – as it further develops its climate-related disclosure expectations for listed companies, asset managers and FCA-regulated asset owners.

What are the key takeaways for organisations?

1. The TPT Framework should not be considered in isolation

The TPT Framework and its associated recommendations have been built to complement the existing climate-related disclosure requirements – including the ISSB’s sustainability disclosure standards (IFRS S1 and IFRS S2)and the Glasgow Financial Alliance for Net Zero (GFANZ) – and focus on the development and disclosure of practical transition plans.

Rather than new guidelines, the TPT Framework provides a more detailed overview of the key elements that should be considered when developing a transition plan.

Figure 1 shows how the coverage of the common areas for climate-related disclosures compares among some of the existing frameworks and sets of requirements. Noticeably, the structure of these sets of requirements is built on some common areas of disclosure, and each framework/initiative focuses on specific aspects that require some degree of integration with the existing sustainability-related reporting.

Figure 1 – Coverage of common climate-related disclosure areas by existing frameworks and initiatives

2. Organisations don’t need to have all the answers to develop a transition plan

While the ultimate goal is to produce a complete and detailed transition plan, the TPT Framework applies to organisations of different maturity levels, and – as stated in their July Status Update – transition planning should be considered as an iterative process, and entities are not expected to provide all the answers in their first plan.

We strongly suggest that organisations make a start and are not put off by the level of detail covered by the TPT Framework. Don’t be put off by a perception that your organisation’s climate-related processes are not mature enough to take on this type of exercise. There is a strong case for doing a dry-run exercise, to test preparedness ahead of these requirements being applied in earnest.

As a practical example of taking a proportionate and incremental approach, within the TPT Framework sub-element 2.4 Financial Planning, firms are expected to disclose quantitative and qualitative information on how they are planning to resource their transition and how its implementation will impact their financial position. As part of this disclosure, the TPT Framework states that organisations should “use all reasonable and supportable information that is available to the entity at the reporting date without undue cost and effort”.

3. Transition plans should not be restricted to addressing the organisation’s decarbonisation plans

While seeking to decarbonise an organisation’s operations and its value chain, the TPT Framework recognises that positive solutions to address opportunities arising from transition, are vital to contributing to guiding the economy through that transition.

There is an implication within the TPT Framework that organisations have the resources and processes to adequately address climate risk, having invested in their risk management function and integrated climate risk considerations into their risk management framework. The ability to provide evidence of strong internal controls over the ultimate disclosures, is an important theme of this and other recent disclosure initiatives, such as IFRS S2.

In relation to contributing to an economy-wide transition, organisations are expected to use the specific levers and capabilities available to them to accelerate the transition to a low-carbon economy. This implies taking a broader strategic perspective on climate change, taking into consideration the opportunities for new or restructured products and services. It also means working with their value chains to ensure the effective adoption of these services.

The wider implications of TPT

We observe that many sustainability teams are struggling to deliver what they are currently being asked to do. The two challenges we are seeing include:

- complexity: organisations are often faced with multiple reporting expectations and an international entity might be regulated by multiple supervisors with varying reporting requirements. Being listed on a major stock exchange brings additional requirements, as do any voluntary commitments the organisation has chosen to make

- speed of change: the rapid evolution of requirements places significant burden on climate teams, with being forced to focus on short-term deadlines. Teams have in some cases been moving from reporting deadline to deadline, without any time to step back and think about how best to be organised.

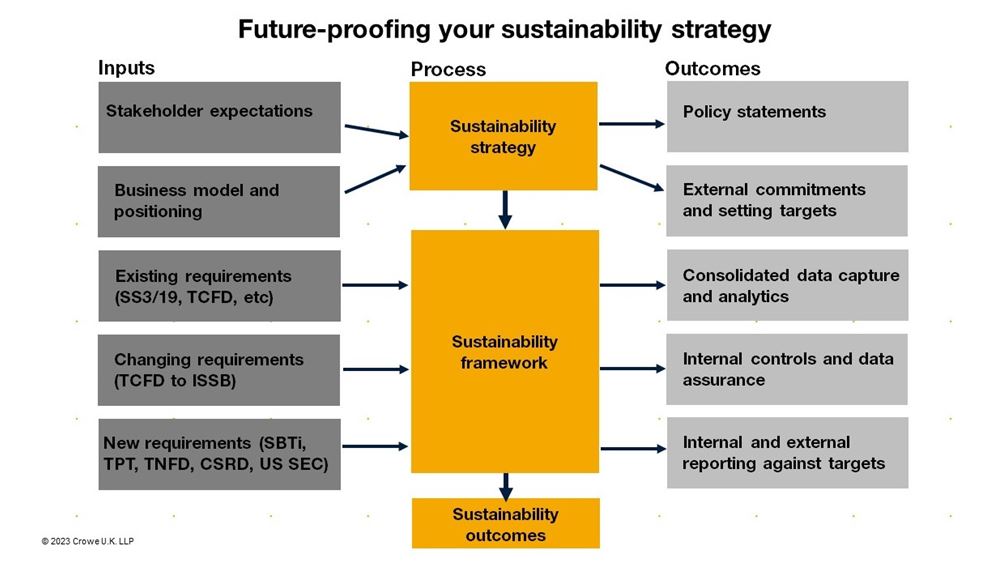

While the first instinct would be to merely integrate the TPT Framework into their existing climate-related disclosures, this new set of recommendations represents an opportunity to think more broadly about the organisation’s sustainability strategy and its related reporting structure.

Figure 2 outlines an example where an organisation firstly puts in place its own sustainability strategy, driven by its strategic context, related to stakeholder and business model. This defines what external commitments and targets are felt to be appropriate. As requirements are modified or added to, the framework is simply adapted and expanded to cope. Now is the time for organisations to step back and think about how best to be organised to manage these requirements.

Figure 2 – Crowe’s approach to addressing rapidly changing sustainability reporting expectations.

While organisations are navigating the challenging climate-related context and are working towards this new set of recommendations for transition planning, it is often helpful to obtain an external perspective on the matter.

At Crowe, we support our clients’ climate journey by:

- providing an overview of the existing frameworks and initiatives, as well as the current market and industry insights

- assisting in the development of their transition plan

- reviewing their transition plan and providing informal and/or formal feedback.

Please contact Alex Hindson or your usual Crowe contact for more information.