Pillar Two

Tax Alert

The OECD/G20 working group agreed on a two-pillar solution to reform international taxation in response to the increasing digitalisation of the economy, focusing on:

- the reallocation of taxing rights (Pillar One); and

- the implementation of a global minimum tax rate of 15% (Pillar Two).

These measures aim to limit base erosion by Large Multinational Groups (LMGs), with groups qualifying for this purpose where their consolidated revenue is equal to or greater than EUR 750 million in two of the last four financial years.

Portugal transposed the European Directive (EU) 2022/2523 (which implements Pillar Two) through Law no. 41/2024, creating the Global Minimum Tax Regime – RIMG (“Global Anti-Base Erosion Tax”, commonly referred to as GloBE) to ensure that large multinational groups are taxed at a minimum effective rate of, in general, 15%:

In summary terms, the regime is based on two interlinked rules intended to determine the “top-up tax” (calculated on a jurisdiction-by-jurisdiction basis) that may be due in cases where an effective tax rate below the aforementioned 15% is identified:

- Income Inclusion Rule (IIR) – intended to allow the jurisdictions of the Ultimate Parent Entities (UPEs) of LMGs to impose a minimum level of taxation on foreign-source profits subject to low taxation — rule applicable to fiscal years beginning on or after 1 January 2024.

- Undertaxed Profits Rule (UTPR) – intended to allow source jurisdictions to prevent the shifting of profits to low-tax jurisdictions — rule applicable to fiscal years beginning on or after 1 January 2025.

To ensure that tax revenue remains in the jurisdiction of the constituent entities of LMGs, an optional mechanism was created allowing the adoption of a “qualified domestic minimum top-up tax regime”. This option has been exercised by Portugal and is referred to as “ICNQ – PT”.

This ICNQ-PT takes precedence over any foreign taxation, ensuring that the tax differential remains within the Portuguese State’s treasury and is not collected by other jurisdictions. Any tax paid in Portugal by local entities will be deductible by the LMG’s parent entity against the tax calculated under the global rules (IIR and UTPR), thereby preventing issues of international double taxation.

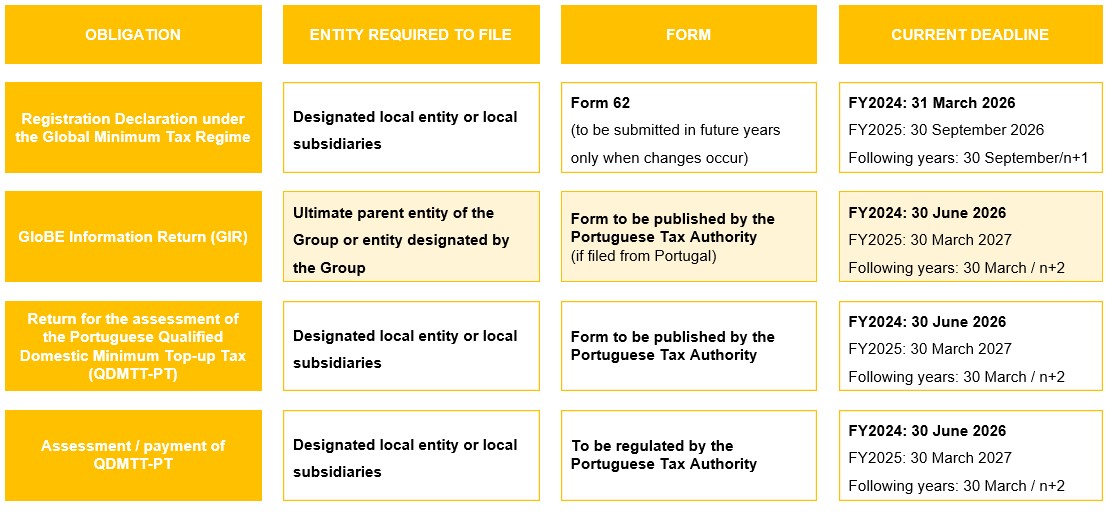

The main reporting obligations and critical deadlines associated with the application of the above-mentioned IIR rule, relating to fiscal years beginning on or after 1 January 2024, which must already be complied with during the current year 2026, are summarised in the table below:

For constituent entities located in Portuguese territory that are subject to an effective tax rate above the aforementioned minimum rate of 15%, or which may apply a safe-harbour regime, it may nevertheless be necessary to submit in Portugal the ICNQ-PT tax assessment return demonstrating this fact, even where the corresponding tax assessment notice is issued with a zero balance (no tax payable). Further regulatory clarification and the publication of the ICNQ-PT return form are currently pending.

Please also note that the deadline for compliance with all the above obligations (with the exception of Form 62, to be submitted by the end of the present month of March) is the same.

Local entities and their parent companies are therefore advised to establish a timetable that allows them, in advance and within the applicable deadlines, to comply properly with the obligations established.

Please note that the failure to submit, or late submission of these returns, may subject entities to significant penalties:

- Failure to submit, or late submission within the statutory deadline, where required, of any mandatory return: from EUR 5,000 to EUR 100,000, with an increase of 5% for each day of delay in fulfilling the obligation.

- Omissions or inaccuracies in the returns: from EUR 500 to EUR 23,500.

The implementation of Pillar Two represents one of the most profound and complex changes in the international tax system in recent decades. The determination of the Effective Tax Rate (ETR) and the calculation of the Top-Up Tax require a detailed analysis that goes far beyond traditional accounting, involving:

- Specific Tax Adjustments: Reconciliation between accounting standards (IFRS/SNC) and the OECD GloBE rules.

- Jurisdiction-Specific Data: The need to collect information from all Group entities within each jurisdiction.

- Safe-Harbour Rules: Verification to determine whether the group may benefit from temporary exemptions in Portugal.