Current guidance

In March 2021, the FASB issued Accounting Standards Update (ASU) No. 2021-03, “Intangibles – Goodwill and Other (Topic 350): Accounting Alternative for Evaluating Triggering Events,” which provides private companies and NFP entities with an accounting alternative to evaluate goodwill triggering events as of the end of the reporting period. This change means these entities may elect to evaluate triggering events only at period-end, removes the need to monitor for triggering events, and eliminates the potential of measuring any related impairment between reporting dates. Multiple market factors could contribute to a triggering event. ASU 2021-03 provides relief for private companies and NFPs as it allows for a period-end retrospective review rather than constant monitoring.

Refresher on goodwill impairment testing

Accounting for goodwill and intangible assets can involve various financial reporting issues, including performing impairment evaluations. Goodwill commonly is booked during purchase accounting following a business combination, reflecting the fair value (FV), or purchase price paid, in excess of the FVs of the identifiable net assets acquired. After goodwill initially has been recorded as an asset, it must be tested for impairment regularly or upon the occurrence of a triggering event. Goodwill impairment occurs when the carrying amount of an entity (its reporting unit or RU) in which goodwill is recorded is greater than its FV. Goodwill impairment testing is covered by Accounting Standards Codification (ASC) 350, “Intangibles – Goodwill and Other.”

Public companies that follow U.S. generally accepted accounting principles, and subsequently ASC 350, are required to perform an impairment analysis test at least annually. Additionally, impairment tests should be performed between annual test dates upon triggering events. FASB guidance under ASU 2021-03 allows certain private and NFP entities electing goodwill amortization accounting to evaluate goodwill impairment triggering events only at the end of each reporting period (whether interim or annual) instead of monitoring for triggering events and potentially measuring any related impairment between reporting dates.

What is a triggering event?

A triggering event is any event or circumstance that indicates that the FV of an entity (or an entity’s RU) might be below its carrying amount. Under ASC 350, goodwill is tested for impairment when one of these triggering events occurs. The following events and circumstances listed in ASC 350-20-35-3C are examples of triggering events:

- Macroeconomic conditions (for example, deterioration in general economy)

- Industry and market considerations (for example, deterioration in the environment in which the entity operates)

- Cost factors (for example, increases in costs of raw materials or labor)

- Overall financial performance (for example, negative or declining cash flows)

- Other relevant entity-specific events (for example, changes in management or key personnel)

- Events affecting an RU (for example, change in composition of net assets or expectation of disposing of all, or a portion of, the RU)

It should be noted that these events and circumstances are examples and not an all-inclusive listing of triggering events. Companies should consider other relevant events and circumstances that might affect their FV or carrying amount of the entity (or RU) when evaluating whether to perform a goodwill impairment test.

As an alternative to a quantitative goodwill impairment test, ASU 2011-08 allows for a qualitative assessment of goodwill impairment for certain entities. As part of this qualitative assessment, an entity must consider whether a greater than 50% likelihood exists that the FV of an entity is less than its carrying value. As part of this determination, companies should consider the previously mentioned triggering events. While management teams can make many of the necessary determinations internally, an independent valuation specialist can provide market and industry data, as well as expert guidance, to produce a robust and auditable qualitative assessment.

What triggering events might be present today?

The listing of potential triggering events included in ASC 350 considers both internal and external factors or conditions that might indicate impairment of a company’s goodwill. In the current market environment, several attributes could represent a triggering event based on their impact to a specific company. Current potential triggering events include:

- Increased market volatility and resulting potential reduction in a corporation’s market capitalization

- Inflation

- Recession

- Global supply chain constraints

- Russia-Ukraine war

All of these events and circumstances could be considered triggering events as outlined in ASC 350-20-35-3C. They represent macroeconomic factors, cost factors, and, for many industries, conditions that could affect the environment in which a company operates.

Companies need to take these current events and circumstances into careful consideration and evaluate their potential impact on goodwill impairment. Is the company experiencing increases in labor and material costs due to inflation or supply chain constraints? Is the company unable or struggling to pass on these costs to customers? How will this affect the company’s projected cash flows and the FV of its RU(s) when testing goodwill impairment?

When it comes time for annual testing, companies should evaluate these events and conditions, along with company-specific performance, in evaluating whether a triggering event has occurred or risk of impairment has increased. Companies also should discuss this information with their external auditors and third-party advisers who assist in the goodwill impairment testing process.

Although it is not explicitly required, publicly traded entities should consider their market capitalization as of the impairment testing date as a corroborative data point in their FV analysis (either a consolidated valuation or the sum of individual reporting segment valuations). In times of heightened market volatility, such an analysis becomes more complex as share prices and industry multiples might increase or decrease significantly over a shortened time horizon, often without specific news or triggering events.

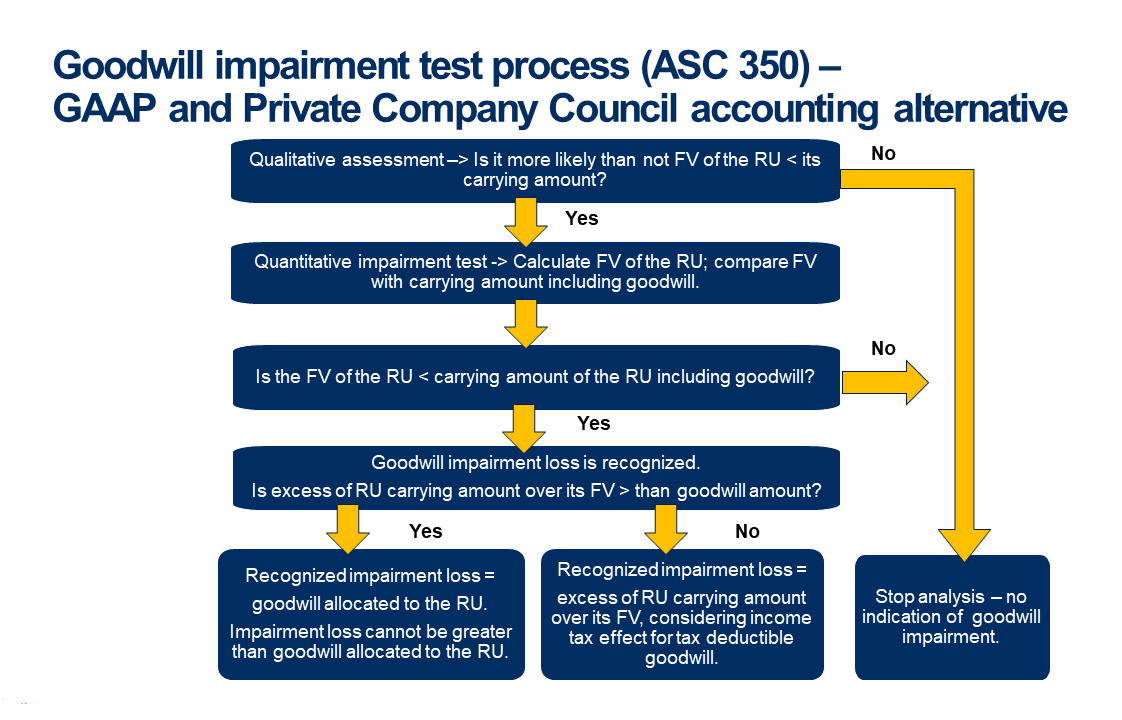

Order of goodwill impairment testing

The test for impairment begins with a qualitative assessment of whether it is “more likely than not” that the FV of the RU is below its carrying amount.1 If the answer is no, then the analysis is complete as there is no indication of goodwill impairment. However, if the answer is yes, then the analysis continues to a quantitative assessment in which the FV of the RU is calculated and compared to the carrying value of the RU. If the FV of the RU is greater than the carrying value of the RU, then the analysis is complete as there is no indication of goodwill impairment. If the FV of the RU is less than the carrying value of the RU including goodwill, then a goodwill impairment loss is recognized. To determine the loss to be recognized, it is necessary to look at the difference between the amount of the carrying value of the RU and the calculated FV of the RU. If the excess of carrying value over FV is greater than the goodwill, then the recognized impairment loss is equal to the goodwill amount as the impairment loss cannot be greater than the goodwill amount allocated to the RU. If the excess is less than the goodwill, then the total excess is recognized as an impairment loss.