ASU 2026-02 Addresses Accounting for Environmental Credits

The Financial Accounting Standards Board (FASB) has issued guidance on accounting for environmental credits.

In under a minute

- On May 19, 2026, the FASB issued Accounting Standards Update (ASU) 2026-02, “Environmental Credits and Environmental Credit Obligations (Topic 818).”

- The standard establishes guidance for accounting for environmental credits and environmental credit obligations (ECOs). The guidance requires recognizing an environmental credit at cost if it is probable that the credit will be used to settle an environmental credit obligation, transferred in an exchange transaction, or used in a nonreciprocal transfer. In addition, the standard requires impairment testing for noncompliance credits as well as liability recognition for environmental credit obligation settlements – with gross balance sheet display.

- The ASU requires enhanced disclosures about an entity’s involvement in environmental credit programs and in events or activities that give rise to ECOs.

- Entities will adopt the standard on a retrospective basis through a cumulative-effect adjustment to the opening retained earnings as of the beginning of the annual reporting period of adoption.

- The update is effective in 2028 for public companies and in 2029 for private companies, with early adoption permitted.

Read more on Take Into Account

This article is from Take Into Account, our accounting advisory knowledge hub offering the latest in accounting standards and financial reporting.

Subscribe to Take Into Account knowledge hub

Background

Navigating the scope, recognition, measurement, presentation, and disclosure of environmental credit programs has been a significant challenge for entities because legacy GAAP lacked explicit guidance. Due to the growing number of entities across various industries engaging in environmental credit programs and arrangements related to climate change initiatives and environmental, social, and governance matters, the FASB added a project to its agenda in May 2022. The resulting ASU provides clear and comprehensive guidance to support consistent and transparent financial reporting for environmental credit programs.

Breaking it down

What is an environmental credit?

An environmental credit is an enforceable right that can be acquired, granted by a regulatory agency, or earned by reducing greenhouse gas emissions, increasing environmental conservation, or using renewable energy sources. An environmental credit also can serve as a permit for emissions, authorizing an entity to generate a specific quantity of emissions. These rights can be bought, sold, or traded.

To be classified as an environmental credit, the credit must:

- Lack physical substance – not be considered a financial asset under GAAP

- Represent the prevention, control, reduction, or removal of emissions or pollutants

- Be separately transferable in an exchange transaction

- Not be classified as an income tax credit to be used to settle an entity’s income tax liability

The guidance also includes credits that are acquired (including from related parties), granted by a regulatory agency or designee, internally generated (created), or received in a nonreciprocal transfer.

Crowe observation: The scope of the guidance excludes tax credits or incentives that are within the scope of Accounting Standards Codification (ASC) 740, “Income Taxes.” When a company receives the benefit of a credit or an incentive based solely on its income or income tax liability, the accounting for the credit is within the scope of ASC 740. In addition, equity investments in income tax credit structures, such as investments in low-income housing tax partnerships or renewable energy tax structures, would be outside the scope of the guidance.

What is an environmental credit obligation?

ECOs are regulatory compliance obligations that arise from existing or enacted laws, statutes, or ordinances represented to prevent, control, reduce, or remove emissions or other pollution that may be settled with environmental credits. Obligations within the scope of Subtopic 410-30, “Environmental Obligations,” are not environmental credit obligations.

Asset recognition and measurement

In recognizing and measuring environmental credits, the ASU uses an intent-based model, focusing on an entity’s intended use of the credits to determine whether they qualify as assets. Determining how to account for an environmental credit involves several considerations.

Initial asset recognition and measurement

An environmental credit is an asset if it is probable that the credit will be used to settle an ECO, transferred in an exchange transaction, or used in a nonreciprocal transfer. If this condition is not met, the environmental credit is not recorded as an asset and should be expensed as incurred unless the credit is required to be accounted for as part of the cost of another asset in accordance with other guidance.

Environmental credits that meet the asset-recognition threshold initially are recorded at acquisition cost. Assets granted by a regulator or generated internally are recorded at cost, limited to transaction costs incurred, if any. Furthermore, any credit acquired in a business combination is recognized as an asset regardless of the intended use and subsequently accounted for in accordance with Topic 818, per ASC 805-20-25-15B. If it is probable that an environmental credit will be used to satisfy an environmental credit obligation, the asset is categorized as a compliance credit. If the credit is not probable to be used to satisfy an ECO, the asset is categorized as a noncompliance credit.

Crowe observation: The master glossary defines a future event as “probable” if it is likely to occur. In practice, “probable” is considered to a be a high threshold to which the event would be deemed to have a 70% or greater likelihood of occurrence.

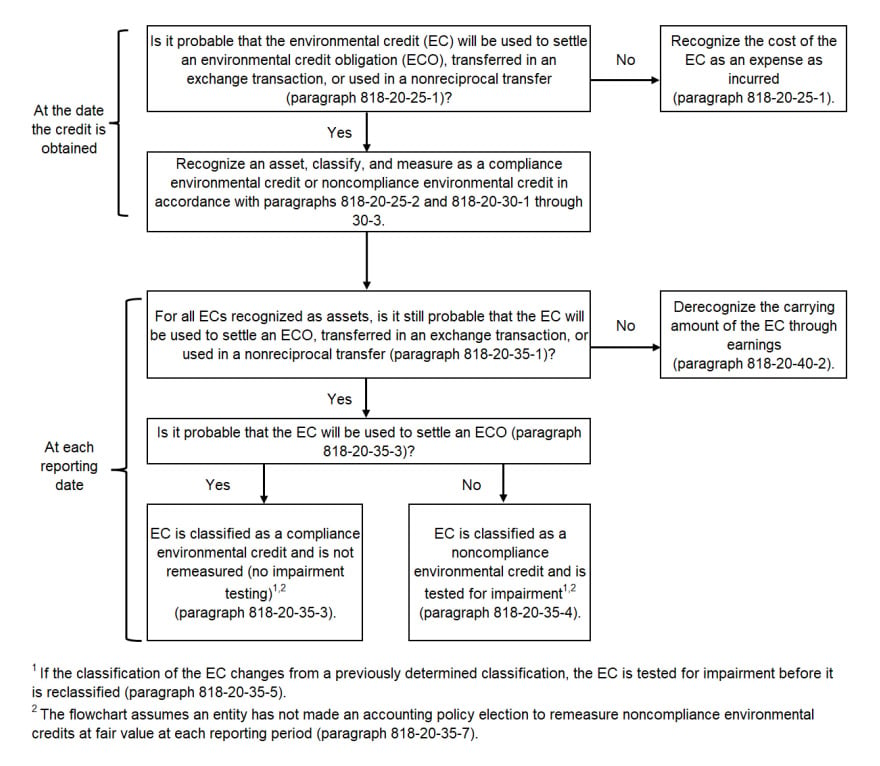

The following flowchart provides an overview of the asset recognition and measurement guidance.

Source: FASB, Accounting Standards Update 2026-02, “Environmental Credits and Environmental Credit Obligations (Topic 818),” p. 34, reprinted with permission.

Subsequent asset measurement

Similar environmental credits recognized as assets are subsequently measured using one of the following cost methods: average cost; first in, first out; or specific identification. Determining subsequent asset measurement is dependent on whether an environmental credit is a compliance credit or a noncompliance credit. Noncompliance credits expected to be sold or traded would be subsequently measured at historical cost less impairment. Impairment should be analyzed at the end of each reporting period and is to be recognized when the carrying value of the noncompliance credit exceeds its fair value. Impairment losses are irreversible. On the other hand, compliance credits are not subsequently remeasured if it remains probable that the environmental credit will be used to settle an ECO. However, if it becomes improbable that the environmental credit will be used to settle an ECO, the asset should be derecognized and reflected in earnings.

Entities must reevaluate compliance and noncompliance classifications at each reporting period. If compliance credits are reclassified to noncompliance credits, an impairment assessment is required.

Crowe observation: Because the intent of compliance credits is to settle ECOs, generally an entity would not realize any gain or loss on the settlement. As such, the board decided not to require subsequent remeasurement at fair value through earnings for compliance credits.

For certain noncompliance credits, an entity is permitted to make a fair value accounting policy election, with changes in fair value recognized in earnings. Credits generated by an entity or received through a grant from a regulator are ineligible for fair value election. The guidance permits an entity, as an accounting policy election, to subsequently measure a class of eligible noncompliance environmental credits at fair value at each reporting date. The entity should determine what constitutes a class based on its facts and circumstances. This election is irrevocable, and the entity must remeasure the asset until derecognition.

Credits that were previously derecognized or never recognized cannot later be recognized as assets.

Liability recognition and measurement

In accordance with the guidance, an entity must recognize a liability when events occurring on or before the balance sheet date indicate the existence of an ECO. When evaluating whether a liability should be recognized, an entity shall determine whether environmental credits would be due assuming that the reporting date is the end of the regulatory compliance period regardless of whether the regulatory compliance period ends after the reporting date.

Entities are not required to recognize liabilities for commitments to purchase environmental credits unless required by other specific guidance in GAAP.

When determining whether to recognize an ECO in a business combination, an entity must assess whether environmental credits would be required assuming the acquisition date represented the end of the regulatory compliance period, even if the actual compliance period extends beyond the acquisition date.

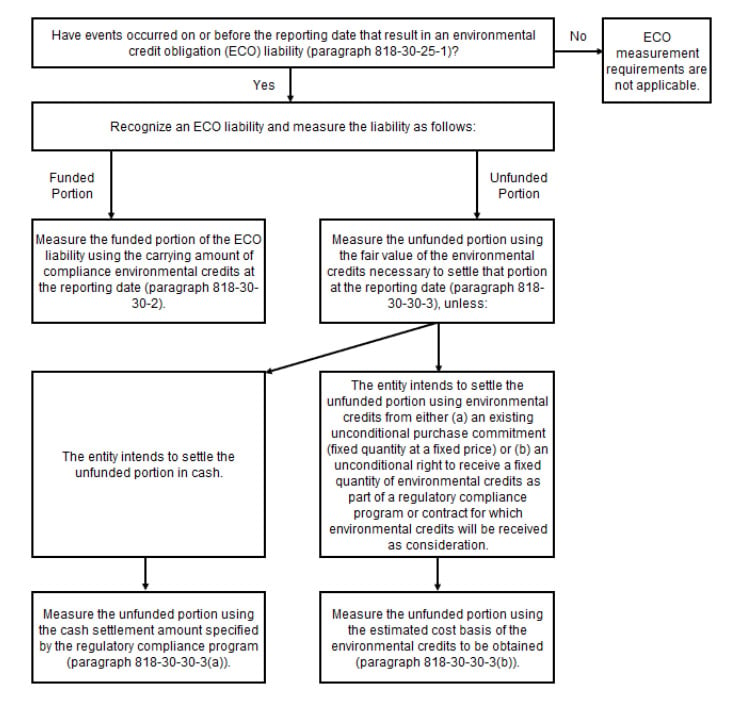

ECO liabilities are measured as follows:

- Funded portion. The funded portion of an ECO refers to the portion of the liability where the entity possesses the credits used to settle ECOs. This portion should be measured at the carrying amount of the credits at the balance sheet’s date.

- Unfunded portion. The unfunded portion represents the residual. This portion should be measured at the fair value of the credits needed to settle the ECO unless the entity intends to settle the ECO using cash. In the case of cash settlement, the liability should be measured based on the costs incurred to obtain the credits. If the settlement is planned through an existing commitment to purchase a fixed quantity of credits at a fixed price or an unconditional right to receive credits as part of a compliance program, the liability is measured based on the estimated cost basis of the credits to be obtained.

The following flowchart provides an overview of ECO recognition and measurement guidance.

Source: FASB, ASU 2026-02, “Environmental Credits and Environmental Credit Obligations (Topic 818),” p. 50, reprinted with permission.

The fair value option under ASC 825 is prohibited for ECO liabilities that can be settled in cash.

Subsequent measurement follows initial requirements, with any changes (including derecognition gains or losses) presented in the same income statement line item as initial recognition.

Presentation and disclosure

Balance sheet presentation

Entities are required to present all environmental credits and ECOs on the balance sheet on a gross basis. The board has decided to prohibit an entity from netting environmental assets and liabilities.

Environmental credits slated for sale, trade, or remittance within the year would be classified as current assets; if not, they would be considered noncurrent assets. Conversely, ECOs due within a year would be considered current liabilities, while those not expected to be settled within a year would be categorized as long-term liabilities.

Income statement presentation

Changes in an ECO should be presented in the income statement in a manner consistent with the recognition and initial measurement of that liability.

Upon derecognition of an ECO, any resulting gain or loss should be presented in the income statement in a manner consistent with the recognition and initial measurement of that liability.

Disclosure

The guidance requires annual disclosure of the types of environmental credits and obligations, information about an entity’s involvement in environmental credit programs, and events or activities that give rise to ECOs or ECOs owned by the entity. The program information disclosed also should include the nature and timing of settlements as well as the entity’s method for subsequently remeasuring both environmental credits recognized as assets and the unfunded portion of ECOs. Significant estimates and judgments that are applied also should be disclosed.

Balance sheet requirements include:

- The carrying amounts as of the balance sheet date of all environmental credits (disaggregated between compliance and noncompliance) and obligations (disaggregated between funded and unfunded)

- For a classified balance sheet, the current and noncurrent balances of compliance environmental credits, noncompliance environmental credits, the funded portion of ECO liabilities, and the unfunded portion of ECO liabilities in addition to disclosure of where those amounts are presented in the consolidated balance sheet (if not separately presented)

Income statement requirements include:

- Total expense recognized for ECOs

- Total expense recognized for environmental credits not initially recognized or subsequently derecognized because it was not probable that those credits would be sold or used to settle an ECO

- Total impairment expense recognized, the nature of the environmental credits that make up that expense, and a description of the facts and circumstances causing the impairment

- The appliable income statement line items or items that include the amounts previously noted

Lastly, annual requirements include disclosure of the total costs associated with an ECO that was capitalized in the carrying amount of another asset in accordance with another topic as well as a description of the asset.

Crowe observation: The board received significant stakeholder feedback strongly supporting the need for enhanced disclosures about an entity’s involvement in environmental credit programs and the financial impacts to the entity’s financial position, results of operations, and cash flows.

Transition and effective dates

Entities adopt the standard on a retrospective basis through a cumulative-effect adjustment to opening retained earnings (or other appropriate components of equity or net assets) as of the beginning of the annual period of adoption. Prior periods are not recast. The update is effective for annual reporting periods beginning after Dec. 15, 2027, and interim reporting periods within those annual reporting periods for public business entities. For all other entities, it is effective for annual reporting periods beginning after Dec. 15, 2028, and interim reporting periods within those annual reporting periods. Early adoption is permitted. If an entity early adopts in an interim period, it must apply the standard as of the beginning of the annual period that includes that interim period.

Measurement of environmental credits at transition depends on the type of credit:

- Entities measure compliance credits at existing carrying value.

- Entities measure noncompliance credits at the lower of carrying value or fair value.

- Entities measure internally generated or regulator-granted credits based on either their intended use or the transaction costs incurred.

- Entities electing the fair value option for a selected class of noncompliance credits must measure those credits at fair value on adoption.

Costs of environmental credits already included in other assets (such as inventory) may remain embedded in those balances after adoption.

New liability guidance (ASC 818-30) must be applied on environmental credit obligations beginning on the adoption date.

FASB materials reprinted with permission. Copyright 2026 by Financial Accounting Foundation, Norwalk, Connecticut. Copyright 1974-1980 by American Institute of Certified Public Accountants.

Contact us

Explore proposed ASC 820 fair value guidance changing investment company reporting to reflect contractual sale restrictions.

FASB proposal to amend ASC 815 by removing barriers to hedge accounting for economically effective hedges.

The SEC has asked for comments by Aug. 3, 2026, on a proposal to withdraw 2024 climate-related disclosure rules and related reporting requirements.

Explore proposed ASC 820 fair value guidance changing investment company reporting to reflect contractual sale restrictions.

FASB proposal to amend ASC 815 by removing barriers to hedge accounting for economically effective hedges.

The SEC has asked for comments by Aug. 3, 2026, on a proposal to withdraw 2024 climate-related disclosure rules and related reporting requirements.