Transfer pricing in the Czech Republic

Fundamental Principle(s) and Legislation

The main objective of transfer pricing is to ensure that transactions between related parties are conducted under the same conditions as would be agreed upon by independent entities in comparable circumstances on the open market. This represents the so-called arm’s length principle.

This principle is codified in Section 23(7) of the Czech Income Tax Act (hereinafter referred to as “ITA”) which requires taxpayers to adjust their tax base if the prices agreed between related parties differ from those that would be agreed upon between unrelated parties in ordinary business relationships under similar or identical conditions, and the difference is not satisfactorily justified. If such a situation results in increase of the tax base, the provision also allows the Czech tax authority to adjust the tax base of the affected taxpayer, for example during a tax audit.

Definition of Related Parties

Under the Czech tax legislation, related parties are those that are financially or otherwise connected. This includes e.g.:

- Parent and subsidiary companies,

- Entities under common control,

- Persons holding at least 25 % of the share capital or voting rights,

- Close persons as defined by the Czech Civil Code (e.g., direct relatives, siblings, spouses, registered partners), and

- Other persons in a family or similar relationship where harm to one would reasonably be perceived as harm to the other.

Additionally, entities are considered related if:

- The same individuals or close persons participate in the management or control of other entities (excluding cases where one person is a member of the supervisory boards of both entities), or

- The legal relationship between the entities was established primarily to reduce the tax base or increase the tax loss.

The definition is quite broad and includes also situations where there is merely the potential to significantly influence the operations or decision-making of another entity.

Transfer Pricing Documentation

Since 2023, there has been increasing emphasis on proper transfer pricing documentation in the Czech Republic. Although not legally mandatory, preparing documentation is highly advisable, especially in the event of a tax audit.

While there is no statutory obligation to prepare transfer pricing documentation, the Czech tax administration has issued several guidelines (known as “D guidelines”) that are binding for the tax authorities and serve as guidance for taxpayers. These include:

- Guideline of General Financial Directorate D-34: Guideline on applying international standards in the taxation of transactions between associated enterprises – transfer pricing,

- Guideline of General Financial Directorate D-32: Guideline on binding assessment of the method used to determine prices between related parties and the method of determining the tax base of a non-resident operating through a permanent establishment,

- Guideline of General Financial Directorate D-10: Guideline on low value-adding intra-group services, and

- Guideline D-334: Ministry of Finance guidance on the scope of documentation for pricing between related parties.

These guidelines largely mirror the OECD Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations and the EU Code of Conduct on transfer pricing documentation.

During the tax audits, the Czech tax authorities focus on the Master file (group-wide overview) and the Local file (detailed documentation of the Czech entity in question). These documents are essential for demonstrating that transactions between related parties comply with the arm’s length principle and for minimizing the risk of tax reassessment.

Approach of the Tax Authorities

Recently, the Czech tax authorities have intensified tax audits focused on transfer pricing. Particular attention is paid to:

- Intra-group services,

- Royalty payments,

- Financial transactions (loans, interest),

- Profit allocation between parent and subsidiary companies.

Such tax audits involve benchmarking analysis of comparable independent transactions, often using public databases (e.g., Amadeus, Orbis), prepared by the tax administrator.

If the tax authority determines that prices do not comply with the arm’s length principle, they may adjust the tax base and assess additional tax, including penalties and interest.

Practice shows that the tax administration increasingly focuses on the economic substance of transactions, i.e. not just on formal requirements of transfer pricing documentation, but whether the transaction reflects standard commercial behaviour.

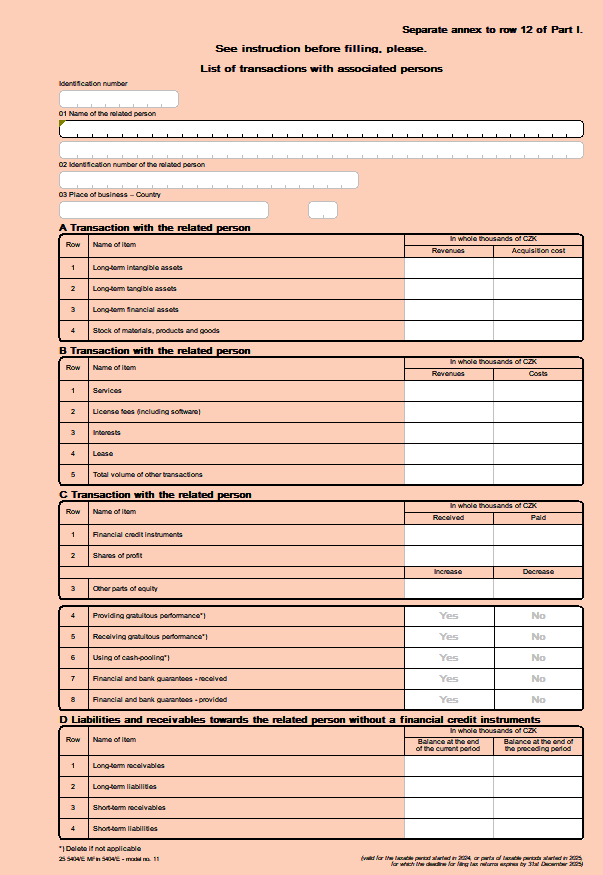

Annex on Transactions with Related Parties

From a practical perspective, it is important to note that corporate income tax returns must include an annex on transactions with related parties. This form contains basic information on the types of transactions, volumes, and whether they were conducted with domestic or foreign related parties.

This annex provides the Czech tax authorities with access to key information on relationships between related entities at the time of filing the tax return.

Taxpayer is required to report transactions with related parties if such taxpayer meets at least one of the following criteria:

- Total assets exceed CZK 40 million,

- Net turnover exceeds CZK 80 million annually,

- Average number of employees exceeds 50.

Additionally, they must meet at least one of the following conditions:

- Conduct transactions with related parties that are tax residents in another country,

- Report a tax loss while conducting transactions with domestic and/or foreign related parties,

- Receive tax relief while conducting transactions with domestic and/or foreign related parties.

Thanks to this annex, the Czech tax administration gains an overview of key transactions between related parties already at the time of filing the tax return. These data are subsequently used for analytical purposes and risk assessment in the selection of entities for audit.

For further information, support or advice on the impact of Amount B on your business, please don’t hesitate to contact us.

Contact our expert