May 2021

In this edition, we have covered the Transfer Pricing updates of Africa, Singapore, Australia, Kenya, Nigeria, Malta and Qatar for the month of May 2021.

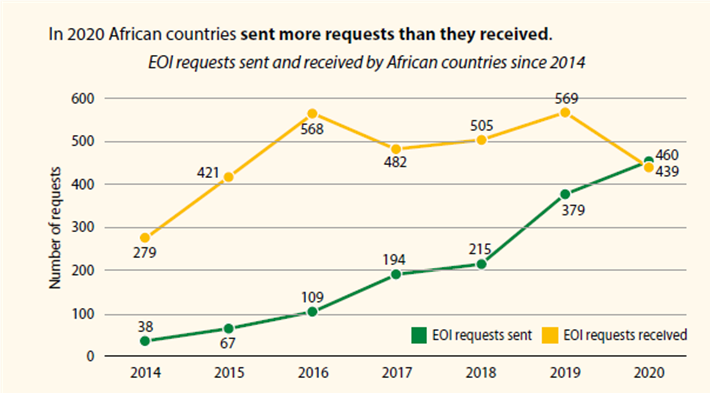

1. Africa – 3rd edition released on Tax Transparency and Exchange of Tax Information

Given the high levels of illicit financial flows from African countries and recognising the potential of tax transparency and exchange of information to raise resources for development, African members of the Global Forum on Transparency and Exchange of Information for Tax Purposes (Global Forum) decided to create an African focused programme: the Africa Initiative in 2014. The objective was to unlock the potential of tax transparency and exchange of information for Africa by ensuring that African countries are equipped to exploit the improvements in global transparency to better tackle tax evasion.

The Africa Initiative is open to all African countries and currently has 32 African member jurisdictions. It is supported by 11 partners and donors.

Recently, 3rd edition (2021) report was published on progress made by African countries (34 countries surveyed) in utilising tax transparency and Exchange of Information (EOI) to tackle tax evasion in 2020.

This report contains six chapters as under:

- Chapter 1 recalls how critical tax transparency is in fighting IFFs in Africa.

- Chapter 2 provides an update of the developments Africa has attained in tax transparency since 2019 and the achievements registered despite the COVID-19 pandemic.

- Chapter 3 measures the progress African jurisdictions registered in 2020 and for the past six years since the Africa Initiative was launched, on the implementation of tax transparency and EOI standards.

- Chapter 4 presents “country safaris”, which share some country experiences in tax transparency and EOI.

- Chapter 5 looks forward to the future of tax transparency in Africa and the work the Africa Initiative intend to focus on to address existing challenges and continue translating tax transparency and EOI into more revenues for Africa’s development, including in the post COVID-19 era.

- Chapter 6 provides a snapshot of the tax transparency and EOI measures introduced by the 34 African countries surveyed and the advancement accomplished.

Source: Tax Transparency in Africa 2021 - Africa Initiative Progress Report

The number of EOI requests sent by African countries in 2020 increased by 21%. For the first time, African countries turned the tide in 2020 and became net senders of EOI requests. However, most African countries are still behind their potential of EOI. More efforts need to be put into the operationalisation of EOI.

African countries identified more than USD 43 million (EUR 34.8 million) in additional taxes due to EOIR in 2020. Since 2009, EOI has enabled African countries to identify over EUR 1.2 billion of additional revenues (tax, interest and penalties).

Crowe UAE’s comments:

African countries are taking significant efforts in increasing tax transparency and exchange of information with the intention to increase their tax revenue. In last decade, many African countries have already issued Transfer Pricing regulations/ guidance and taking actions to implement the same effectively.

Therefore, both companies headquartered in Africa or foreign multinational group having presence in Africa needs to revisit their operational structure to align with Transfer Pricing principles to mitigate the risks.

2. Singapore-Transfer Pricing Guidelines for centralised activities

Recently, Inland Revenue Authority of Singapore (IRAS), has issued Transfer Pricing guidelines for centralised activities of multinational group in Singapore. Guidelines not only focus on large number of headquarters situated in Singapore but also include other entities who provide centralised services to their group entities.

We have summarised the key points of the guidelines as under:

1. It is clarified that there are diverse functional profiles of headquarters which define their contribution to value chain analysis. It is imperative to evaluate the operations of the Group and accurately delineate the intra-group transaction in order to determine the intensity of activities undertaken by headquarters, and the corresponding arm’s length transfer price.

2. Guidelines discusses four categories of activities undertaken by headquarters such as

- Principal in distribution, manufacturing or research and development arrangements;

- Activities relating to core business processes;

- Activities relating to administrative, technical, financial, commercial, management, coordination and control functions);

3. Guidelines has emphasized on robust functional analysis having regard to the characterisation of the headquarter entity and basis that appropriate transfer pricing methodologies may be adopted.

Crowe UAE’s comments:

Intra-group service charge or management fees is one of the most prone transfer pricing issue across world. In multinational group structure, it is quite routine to have such kind of cross charge for centralised activities provided by headquarter. In most countries, tax authority always challenges such cross charge on account of following:

- Whether any actual services were availed by taxpayer?

- Whether services are received are duplicative in nature?

- Whether activities are akin to shareholders activities? If yes, whether charges were required to be paid?

- Whether mark-up on such cost were required to be paid? Can this be considered as pure cost to cost arrangement?

- What is the arm’s length value of charges paid by taxpayer?

Guidance provided by IRAS will certainly help taxpayers in evaluating the intra-group arrangement in detail and determining appropriate arm’s length price. Having said this, taxpayers are recommended to document robust analysis to justify at later stage.

3. Australia-ATO released draft guidelines on intangible arrangements

Recently, Australia Tax Officer (ATO) has released PCG 2021/D4, a draft Practical Compliance Guideline, in relation to cross-border intra-group arrangements of intangibles. We have summarised key findings of the guidelines as under:

1. Draft guidelines covers all types of intangible arrangement, including but not limited to

- Transfer of acquisition of intangible assets

- Licensing of intangibles assets

- Development, Enhancement, Maintenance, Protection and Exploration (DEMPE) functions of intangible assets

- Characterization of transaction

2. Further, guidance focuses not only transfer pricing risk of intangible but also other Australian tax laws that may be relevant, including capital gains tax, withholding tax, the general anti-avoidance rules (GAAR) and diverted profits tax (DPT).

3. Draft guidelines provides a framework as to how ATO examines intangible arrangements and categorises in high, medium or low risk. Additionally, taxpayers having intra-group intangible transaction may need to furnish Reportable Tax Position (RTP) Schedule along with annual income tax return and may also need to self-assess the risk relating to intangible in RTP disclosures.

Crowe UAE’s comments:

Over the years, ATO is considered to be one of the most aggressive transfer pricing authorities in terms of issuing guidance to taxpayers as well as scrutinizing intra-group transactions. Frequent guidance on complex issues published by ATO shows their seriousness in ensuring Transfer Pricing compliance in a country.

Moreover, it is often a complex exercise to determine arm’s length price for intangible arrangements and it is advisable to undertake detailed exercise to evaluate DEMPE functions of entities involved in the transactions. While this draft guidelines will certainly help to taxpayers, self assessment of risk may trigger challenges. We recommend taxpayers to prepare/ maintain robust analysis for intangible transactions including benchmarking analysis to demonstrate fair allocation of profitability.

4. Kenya-Proposed Country by Country Reporting Regulation

On 5th May 2021, Kenya has introduced Finance Bill 2021 (the Bill) before reading the budget in June 2021. Amongst other tax related amendments proposed, the Bill proposed requirement for multinational group to submit group’s financial activities in Kenya as well as other countries. This is akin to country by country (CbC) report.

The information required to be submitted by the ultimate parent entity would include jurisdiction-wise amount of revenue, profit or loss before tax, income tax paid, income tax accrued, stated capital, accumulated earnings, number of employees and tangible assets other than cash or cash equivalents for all the jurisdictions where the group has presence.

The return would be required to be submitted not later than 12 months from the last day of the group’s financial year and it is proposed to commence the regulation from 1st January 2022. Interestingly, turnover threshold for applicability of Regulation is yet to be provided.

Crowe UAE’s comments:

While Kenya is a signatory to Organisation of Economic Co-Operation and Development’s (OECD) Inclusive Framework on Base Erosion and Profit Shifting (BEPS), it has not yet signed Multilateral Competent Authority Agreement on Country by Country Report. Having said this, it is learnt that Kenya is progressing on ensuring Transfer Pricing requirement in country and tax authority too scrutinizing the case to evaluate profit shifting cases.

With the proposed introduction of CbC Reporting Regulation, the taxpayers are required to prepare additional transfer pricing documentation (if applicable) and therefore, it is recommended to relook their intra-group transactions policy at early stage to avoid challenges in future.

5. Nigeria-Suspension of Country by Country Report for subsidiaries and branches

In 2018, Federal Inland Revenue Service (FIRS) of Nigeria has published The Income Tax (Country by Country Reporting) Regulations S.I. No. 6 of 2018. Based on this, subject to revenue threshold, following persons were required to submit CbC Report in Nigeria:

- Ultimate Parent entity of multinational group headquartered in Nigeria;

- Nigerian branches/ subsidiaries of foreign multinational group - when there is no automatic exchange of information mechanism between Nigeria and country of ultimate parent entity

However, recently, FIRS has issued a public notice suspending CbC obligation for Nigerian branches/ subsidiaries of multinational group. Having said this, these entities are required to continue to comply filing of annual notification under CbC Regulations.

Further, filing obligation of ultimate parent entity of multinational group headquartered in Nigeria will remain continue.

Crowe UAE’s comments:

The above suspension of CbC report filing obligations of Nigerian branches and subsidiaries will reduce the compliance burden significantly.

Further, this step is in alignment of Nigeria’s current status as a “non-reciprocal jurisdiction.” In other words, as a non-reciprocal jurisdiction, while Nigeria has agreed to provide CbC reports to other countries, it does not intend to receive any CbC reports from other countries.

6. Malta-Penalty for Country by Country Reporting non-compliance

Malta has published amendment in Cooperation with Other Jurisdictions on Tax Matters (Amendment) Regulations, 2021 wherein it has introduced penalty provisions for non-compliance of CbC Reporting regulations.

As per Malta CbC Reporting Regulations, all constituent entities are required to submit notification whether their multinational group is required to file CbC Report and if yes, jurisdiction in which multinational group is filing the report. This notification is required to be filed on or before last day of filing tax return of Malta constituent entity for preceding fiscal year.

Recently, Malta authority has provided that failure to notify/ inform that which entity entity will be filing CbC Report or whether constituent entity falls under the obligation to file the CbC Report will invite penalty of Euro 200 and Euro 50 for every day of non-compliance to each stated obligation separately. Having said this, total penalty is restricted at Euro 5,000 for each non-compliance activity.

Crowe UAE’s comments:

African countries are significantly progressing towards achieving tax transparency and with this intention, countries are adopting stricter norms in implementing transfer pricing provisions in country.

7. Qatar-Published FAQs on Transfer Pricing documentation

Earlier in December 2019, Qatar’s General Tax Authority (GTA) has issued Executive Regulation to Law No. 24 of 2018 by way of Decision No. 39 of 2019 published on 11th December 2019 introducing substantive changes in Tax and Transfer Pricing Regulation.

Subsequently, GTA has issued additional Transfer Pricing guidance on documentation and compliance requirement by way of President’s Decision No. 4 of 2020.

Recently, GTA has released Frequently Asked Question (FAQ) to address the concerns of taxpayer on Transfer Pricing Regulation. FAQ is dividend in two parts i.e. (1) Transfer Pricing declaration form (2) local file and master file documentation.

Click here to read our detailed alert providing insights on FAQs.

Crowe UAE’s comments:

Qatar, in line with other Middle East and Africa countries, are frequently providing guidance for taxpayers before their first compliance for FY 2020 due in 30th June 2021. FAQ’s are a welcome step to provide much needed clarity to taxpayers. Now, the taxpayers in Qatar are recommended to –

- Conduct a health-check for their intra-group transaction (domestic or cross-border) keeping in mind requirements of Transfer Pricing Regulation

- Take corrective steps, basis the risk areas identified during the health-check

Ensure accurate/ appropriate disclosures to be submitted in Transfer Pricing Declaration form and local file/ master file documentation within prescribed time.