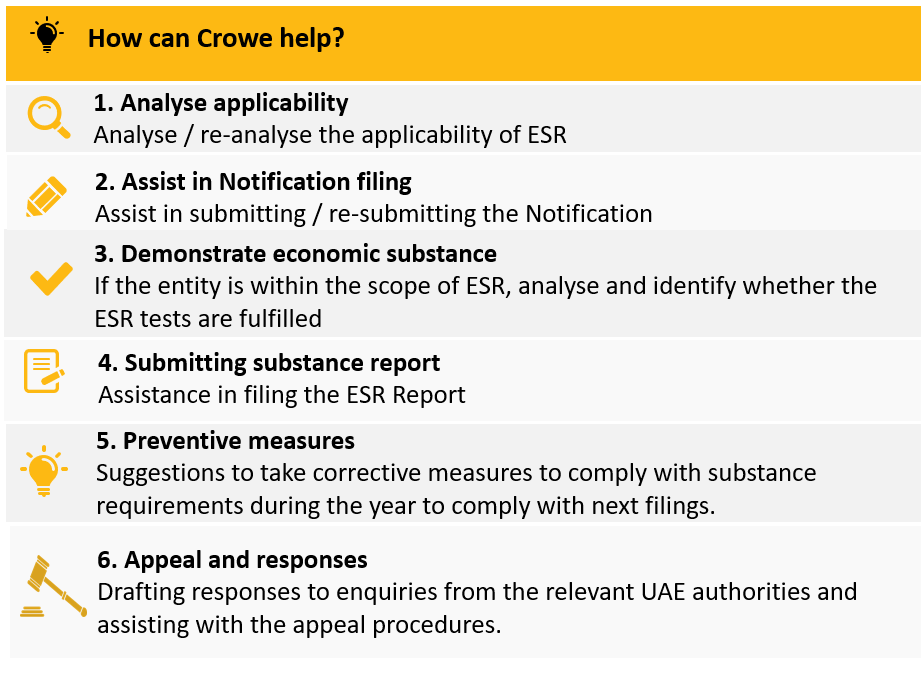

Economic Substance Regulation - Update

In 2019 the UAE introduced the Economic Substance Regulation (‘ESR’) for specific activities in accordance with BEPS Action Plan 5 to discourage shifting of income to low or nominal tax countries.

On 31 March 2021, the OECD has issued a publication stating that the first tax information exchange under the Forum on Harmful Tax Practice’s (FHTP) global standard on substantial activities is initiated for several no or nominal tax jurisdictions including the UAE.

The exchange of information includes the identity, activities and ownership of entities. The exchange of information may enable the receiving tax administrations to carry out risk assessments and to apply their controlled-foreign company, transfer pricing and other anti-base erosion and profit shifting provisions.

Impact:

As most of the first filings for ESR are completed, the Federal Tax Authority has started assessing the compliance of UAE businesses with the substance rules. Non-compliance with substance requirements, engaging in intellectual property or other high-risk activities may result in the exchange of information with foreign authorities by the UAE authorities.

UAE based companies should be mindful of when their information can be exchanged with foreign authorities by the UAE. Such companies should fulfil their obligations under the ESR to avoid tax assessments in other jurisdictions where they have presence.