The financial reporting implications of mandatory accounting standards for NFPs

There are two accounting standards that mandatorily apply from 1 July 2021 that are raising a number of questions for preparers of financial statements:

- AASB 2020-2 Amendments to Australian Accounting Standards – Removal of Special Purpose Financial Statements for Certain For-Profit Private Sector Entities (AASB 2020-2)

- AASB 1060 General Purpose Financial Statements – Simplified Disclosures for For-Profit and Not-for-Profit Tier 2 Entities (AASB 1060)

To help you understand how Not-for-profit (NFP) entities may be impacted, we’ve prepared some Frequently Asked Questions (FAQs) and a downloadable table outlining the disclosure differences between general purpose financial statements (GPFS) prepared under the new AASB 1060 and GPFS prepared under the current RDR framework.

Can NFPs still prepare special purpose financial statements?

Yes. You have a choice to prepare either special purpose or general purpose financial statements as AASB 2020-2 does not apply to NFPs. However, if the NFP entity is a reporting entity as defined by the accounting standards then you need to prepare general purpose financial statements.

A reporting entity is defined in AASB 1053 Application of Tiers of Australian Accounting Standards as 'an entity in respect of which it is reasonable to expect the existence of users who rely on the entity's general purpose financial statements for information that will be useful to them for making and evaluating decisions about the allocation of resources. A reporting entity can be a single entity or a group comprising a parent and all of its subsidiaries'.

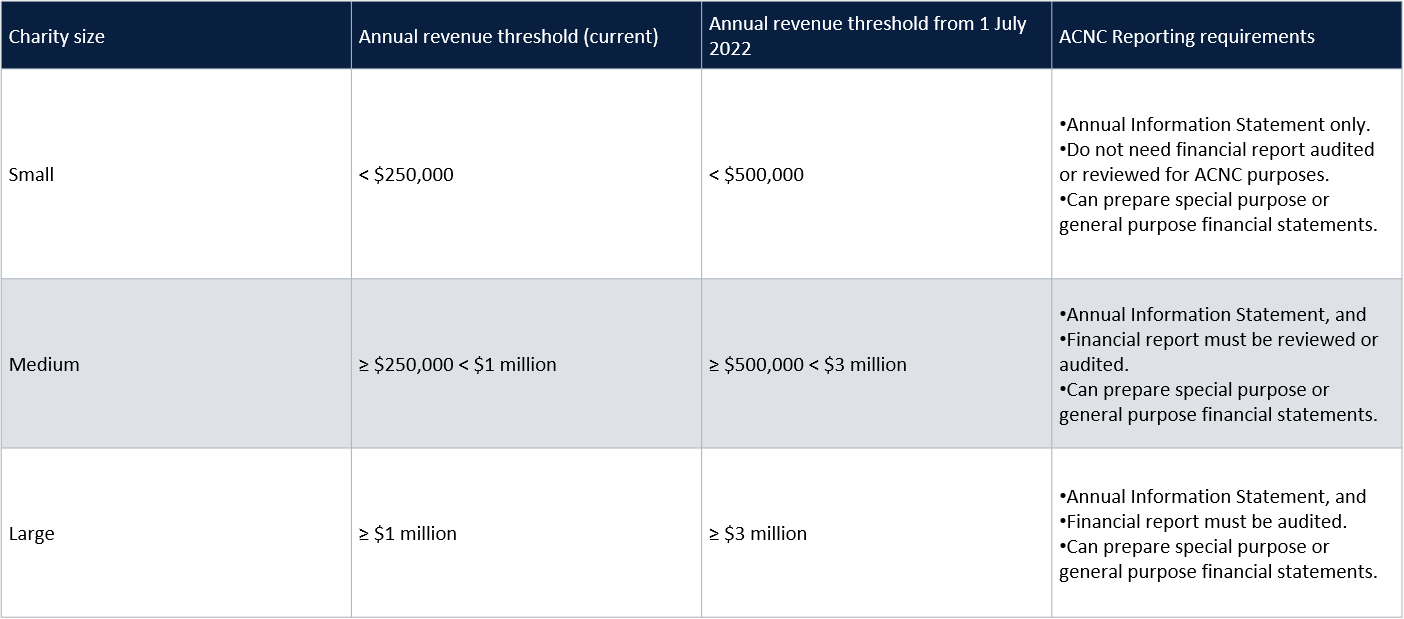

If you are required to report to the Australian Charities and Not-for-Profits Commission (ACNC), your reporting obligations are based on your charity’s size.

The current and revised thresholds from 1 July 2022 are outlined below:

What Accounting Standards do NFPs need to comply with?

If special purpose financial statements are prepared, the ACNC requires compliance with the following accounting standards, at a minimum:

- AASB 101 Presentation of Financial Statements.

- AASB 107 Statement of Cash Flows.

- AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors.

- AASB 1048 Interpretation of Standards.

- AASB 1054 Australian additional disclosures.

What disclosures do NFPs need to be careful not to overlook?

If applicable, AASB 1054 Australian additional disclosures requires private sector NFPs to clearly disclose the following:

- Why special purpose financial statements have been prepared.

- Whether subsidiaries and investments in associates or joint ventures have been consolidated or equity accounted in accordance with AASB 10 Consolidated Financial Statements or AASB 128 Investments in Associates and Joint Ventures.

- An indication of how the entity does not comply where there is non-compliance with material recognition and measurement requirements of AASBs. If an assessment has not been made, this should be disclosed.

- Overall compliance with recognition and measurement requirements of AASBs.

What about NFPs that prepare general purpose financial statements under the reduced disclosure regime?

AASB 1060 is a stand-alone disclosure standard that replaces the current Tier 2 Reduced Disclosure Requirements (RDR) framework. It applies to all entities reporting under Tier 2 of the Differential Reporting Framework in AASB 1053. The standard is effective for annual reporting periods beginning on or after 1 July 2021.

AASB 1060 is a single standard containing all the disclosures required by entities applying Tier 2 reporting.

The following special transitional relief applies if AASB 1060 is applied early:

- Comparatives for those note disclosures that were not previously required for RDR are not required.

Early adoption of AASB 1060 is encouraged as the above relief is not available if the standard is not adopted until the mandatory date of 1 July 2021.

What are the disclosure differences between general purpose financial statements (GPFS) prepared under the new AASB 1060 and GPFS prepared under the current RDR framework?

General purpose financial statements (GPFS) prepared under the new AASB 1060 and GPFS prepared under the current RDR framework will require significant disclosure differences. This summary provides an overview of the major differences. It does not analyse the disclosures that can be removed, nor is it an exhaustive list of all differences that exist.

Financial statement preparation for NFPs is a complex area so it’s important to seek advice to help ensure you are complying with the relevant rules and legislation. Please speak to your adviser for assistance or get in touch with the Crowe External Audit team.