Sustainability reporting in Australia: a practical guide for corporates

Introduction

Sustainability reporting in Australia is undergoing a fundamental shift. What was once largely voluntary and narrative-based is now becoming a regulated, assurance-ready component of corporate reporting. For Australian organisations, this change represents both a compliance obligation and an opportunity to strengthen governance, risk management and long-term value creation.At Crowe, we see sustainability reporting not as a standalone exercise, but as part of an integrated approach to strategy, risk and performance. The new Australian requirements bring climate-related financial disclosures into the core of financial reporting and director accountability, requiring practical, commercially grounded responses. This article provides a clear overview of the sustainability reporting landscape in Australia, outlines what the legislation requires, explains the relevant accounting standards, and highlights how organisations can prepare. It also sets out how Crowe supports clients through this transition.

The sustainability reporting landscape in Australia

Australia’s sustainability reporting framework is being implemented through amendments to the Corporations Act 2001, supported by new Australian Sustainability Reporting Standards issued by the Australian Accounting Standards Board (AASB). The reforms are broadly aligned with the International Sustainability Standards Board (ISSB) standards and are intended to provide investors and other users with consistent, comparable and decision useful information about climate related risks and opportunities.Initially, the mandatory focus is on climate related financial disclosures. However, the broader architecture has been designed to expand over time to other sustainability topics as standards are developed.

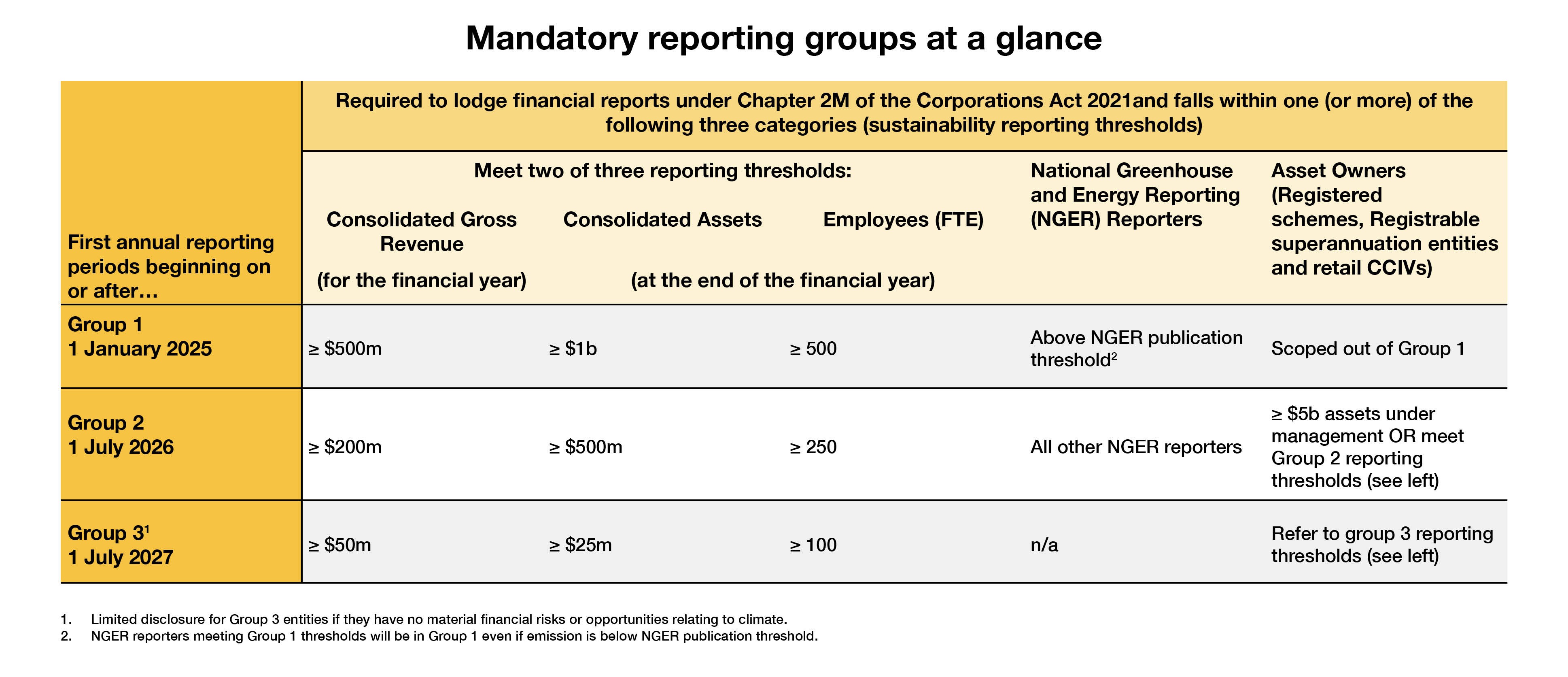

Legislative requirements and entity groupings

The Australian Government has introduced a phased approach to mandatory sustainability reporting through amendments to the Corporations Act 2001. The regime focuses initially on climate-related financial disclosures and applies to entities based on size and economic significance.

This staged implementation recognises differing levels of organisational readiness while signalling a clear direction of travel for all Australian corporates.

As can be seen from the table above, the Group 3 threshold is the same thresholds as Corps Act “large proprietary company”, requiring mandatory financial reporting to ASIC. However, if a Group 3 entity does not have material climate risks and opportunities, they are exempt from preparing a full sustainability report. Instead, these entities need to make a disclosure of a statement that they do not have material climate risks and opportunities, and the reasons why.

ASIC has also clarified that the sustainability reporting requirements crystalises at the end of the financial year. Entities should establish adequate systems to assess whether they may be required to prepare a sustainability report, even if they do not meet the sustainability reporting thresholds at the commencement of that financial year. For example, an acquisition or corporate restructure may occur during the year resulting in a change to the entity’s reporting status.

Contents of the report

A reporting entity’s annual sustainability report for a financial year consists of:

- the climate statements;

- the notes to the climate statements; and

- the directors’ declaration about the climate statements and notes.

Climate statements must comply with the Corporations Act and AASB S2 Climate-related Disclosures. Under section 296D, entities are required to disclose:

- material climate-related financial risks and opportunities,

- relevant climate metrics and targets (including Scope 1, 2 and 3 emissions); and

- information on governance, strategy and risk management.

These disclosures are determined in accordance with AASB S2 Climate-related financial disclosures.

Timing of reporting

The report must be provided to the members and lodged with ASIC no later than:

- three months after the end of the financial year (for disclosing entities, RSEs and registered schemes); or

- four months after the year end for all other reporting entities.

Relevant accounting standards: AASB S1 and AASB S2

The mandatory reporting regime is underpinned by two Australian Sustainability Reporting Standards issued by the AASB.

AASB S1 – General requirements for disclosure of sustainability-related financial information

AASB S1 provides the overarching framework for sustainability-related financial disclosures. It establishes principles for identifying and disclosing sustainability-related risks and opportunities that could reasonably be expected to affect an entity’s cash flows, access to finance or cost of capital over the short, medium or long term.

Although AASB S1 is not currently mandatory on a standalone basis, it sets the foundation for climate reporting under AASB S2 and future sustainability standards.

AASB S2 – Climate-related financial disclosures

AASB S2 is the primary mandatory standard under the first phase of the Australian regime. It requires entities to disclose decision-useful information about climate-related risks and opportunities that may affect enterprise value.

The standard builds on the Task Force on Climate-related Financial Disclosures (TCFD) framework and reflects global investor expectations for consistent, comparable climate information.

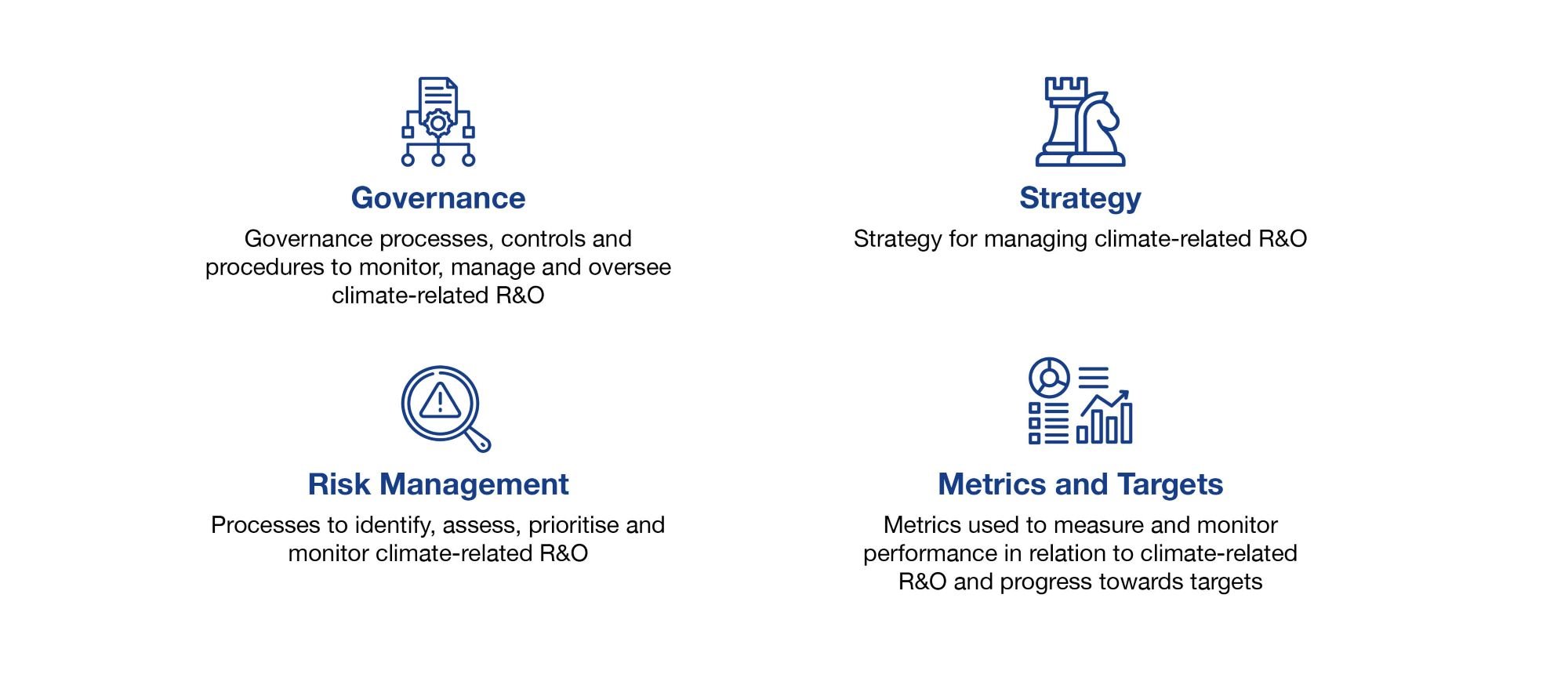

Overview of AASB S2: the four disclosure pillars

AASB S2 is structured around four core pillars. Together, these pillars require organisations to demonstrate that considerations over climate-related risk and opportunities are embedded into governance, strategy, risk management and performance measurement.

Governance

Entities must explain how climate-related risks and opportunities are governed, including:

- How responsibilities for climate-related risks and opportunities are reflected in the terms of reference, mandates and role descriptions of the governance bodies or individuals.

- How the bodies or individuals determine whether the entity has people with the right skills and competencies, or whether these should be developed, to oversee its strategies.

- Management’s role in the governance processes, controls and procedures used to monitor, manage and oversee climate-related risks and opportunities.

From a regulatory and assurance perspective, this pillar reinforces the importance of director capability, documented oversight and clear reporting lines.

Strategy

Climate-related risks and opportunities can affect how an entity sets its strategy and makes decisions. To help investors understand the effects of climate-related risks and opportunities on an entity’s strategy and decision-making, the entity is required to disclose information about:

- Current and anticipated changes to its business model.

- Current and anticipated direct and indirect adaptation or mitigation efforts.

- Plans, if it has any, to transition to a lower-carbon economy.

- How it plans to achieve its climate-related targets.

- How it is currently resourcing, or plans to resource, its response to climate-related risks and opportunities.

- Quantitative and qualitative information about the progress of plans disclosed in previous reporting periods.

A key element of the “strategy pillar” involves the disclosure of how resilient an entity is in the face of climate-related risks. AASB S2 requires all entities to use climate-related scenario analysis to inform their disclosure about their resilience to climate change. Section 296D of the Corporations Act 2001 requires a minimum of two scenarios to be analysed:

(i) The increase in global average temperatures is limited to the increase mentioned in subparagraph 3(a)(i) of the Climate Change Act 2022, currently 1.5°C above pre-industrial levels.

(ii) The increase in global average temperatures well exceeds the increase mentioned in subparagraph 3(a)(ii) of the Climate Change Act 2022 currently 2°C above pre-industrial levels.

This moves climate from a sustainability discussion into core strategic and financial decision-making.

Risk management

Organisations must describe how climate-related risks are identified, assessed and managed, and how these processes are integrated into the broader risk management framework.

Consistency between climate risk processes and existing risk governance will be a key area of regulatory and assurance focus.

Metrics and targets

This pillar requires disclosure of:

- Scope 1 and scope 2 greenhouse gas emissions in year one, with scope 3 introduced from year two onwards.

- Metrics used to assess climate-related risks and opportunities.

- Targets set and performance against those targets.

For many organisations, this may represent the most operationally challenging aspect of reporting.

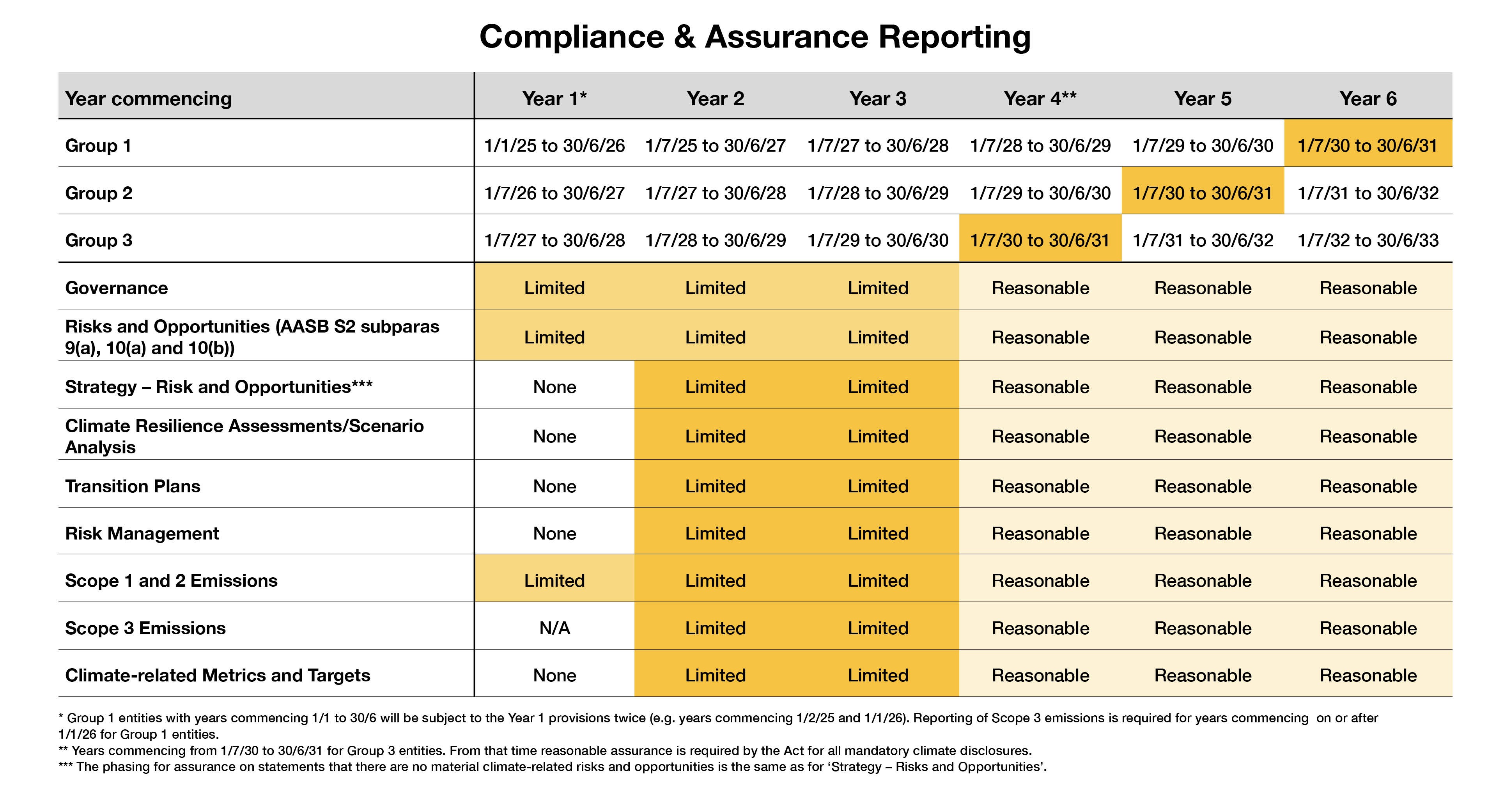

Assurance requirements and phasing

Assurance over sustainability disclosures will be introduced progressively, reflecting the increasing maturity of reporting practices.

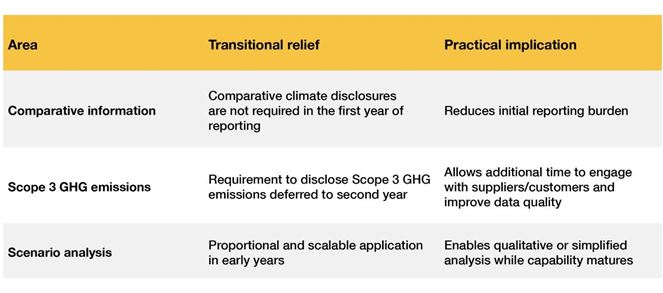

Transitional relief

Recognising the scale and complexity of implementing climate-related financial disclosures, AASB S2 includes a range of transitional reliefs. These reliefs are designed to support entities as they build capability, systems and data quality, while maintaining a clear pathway to full compliance.

What should directors and management do now?

Directors and management play a central role in ensuring that sustainability reporting is credible, decision-useful and proportionate.

Key actions include:

- Mobilise a working group – Establish a cross functional working group across finance, strategy, sustainability, risk, legal, procurement, operations, etc with executive sponsorship and a shared goal.

- Understand responsibilities – Ensure the board and executive team clearly understand the legislative requirements, the standards and their accountability.

- Confirm reporting scope and timing – Determine the entity’s reporting group and commencement date, including any transitional reliefs.

- Perform a structured gap analysis – Assess current governance, strategy, risk and data processes against AASB S2 requirements.

- Strengthen governance frameworks – Clarify ownership, reporting lines and escalation processes for climate-related matters.

- Invest in data and systems early – Establish robust emissions measurement, documentation and internal controls.

- Embed climate into strategy and risk – Integrate climate considerations into enterprise risk management, capital allocation and strategic planning.

- Plan for assurance – Engage early with assurance providers to understand expectations and avoid late-stage remediation.

Early preparation reduces compliance risk and enables organisations to derive strategic value from sustainability reporting.

How Crowe supports clients

Crowe supports organisations across the sustainability reporting journey, from initial readiness to ongoing compliance and assurance.

Our support includes:

- Governance and framework design, including board and management roles and policies.

- AASB S2-aligned gap analyses and implementation roadmaps.

- Emissions measurement and data advisory, including systems, controls and documentation.

- Integration of climate risk into strategy and enterprise risk management.

- Pre-assurance and assurance readiness support, working closely with your auditors.

- Public and private sustainability assurance, both limited and/or reasonable assurance.

Our approach is practical, proportionate and tailored to the size, complexity and maturity of each organisation. We focus on helping clients meet regulatory requirements while strengthening decision-making and long-term resilience.

Conclusion

Australia’s sustainability reporting reforms represent a significant shift in corporate reporting and governance. Climate-related financial disclosures are becoming a core component of financial reporting, director oversight and stakeholder confidence.

Organisations that act early, take a structured approach and leverage experienced advisors will be better positioned to manage risk, meet regulatory expectations and build sustainable value. Crowe works alongside clients to navigate this change with clarity, confidence and commercial insight.