Payday superannuation: what employers need to know

20/03/2026

Big changes are coming to the way superannuation contributions work. If you employ people, it’s time to start preparing.

With the passing of the Treasury Laws Amendment (Payday Superannuation) Bill 2025 (Cth) and the Superannuation Guarantee Charge Amendment Bill 2025 (Cth), employers will be required to pay superannuation at the same time as salaries and wages, starting 1 July 2026. The idea is simple: more frequent contributions mean problems like underpayment or non-payment can be caught much sooner.

We won’t sugarcoat it — the timeline is tight. Many employers, particularly small businesses, have raised concerns about the amount of time available to update systems and processes. That’s exactly why it’s worth starting to plan now rather than later.

There’s also one more matter to be aware of: the Small Business Superannuation Clearing House will close permanently on 1 July 2026. If you currently use it, you’ll need to find an alternative provider before then.

What’s changing

Qualifying earnings

At the moment, super contributions can be calculated using one of two earnings bases: ordinary time earnings or ‘salary or wages’. Under the new rules, both will be replaced by a single concept called Qualifying Earnings (QE). This applies both when working out whether a Superannuation Guarantee (SG) shortfall has occurred, and when calculating the Superannuation Guarantee Charge (SGC) if a shortfall does arise.

Qualifying earnings will include:

- the employee’s ordinary time earnings;

- superannuation contributions from salary sacrifice arrangements. Importantly, amounts sacrificed will still count towards QE, so employees won’t end up with less super as a result of their salary sacrifice arrangement; and

- other amounts included in an employee’s pay, such as commissions, payments for board-level executive duties, and payments under certain types of services contracts.

You can find more detail on qualifying earnings on the ATO website.

Timing of contribution payments

Under the new framework, your obligation to contribute arises on the “QE day”, which is simply the day you pay your employee their qualifying earnings.

To count as an eligible contribution, the super payment must be received by the fund and be ready to allocate within seven business days of the QE day. If that window is missed, the employer is responsible — not the clearing house or the super fund.

For new starters, the same seven-business-day rule applies to regular payments. Their very first contribution, however, gets a slightly more generous deadline of 20 business days.

Allocation of funds

Once a super fund receives an employer contribution and the required information, it must allocate the funds to the employee’s account as soon as practicable and no later than three business days.

One thing to watch: the contribution must be able to be allocated, meaning the fund needs to be able to identify the member and match the payment to an active account. If a contribution gets rejected — say, because the wrong TFN was provided — it won’t count as an eligible contribution, and you’ll have an SG shortfall on your hands. Good data hygiene in your payroll system goes a long way here.

How the Superannuation Guarantee Charge is calculated

You’ll be liable for the Superannuation Guarantee Charge (SGC) if you have an SG shortfall either because a contribution wasn’t made on time, or because you haven’t complied with the choice of fund requirements.

The SGC is made up of:

- the total of your individual final SG shortfalls for the QE day;

- daily interest accruing on those shortfalls until the late payment is made (‘individual notional earnings components’);

- an administrative uplift starting at 60% of the combined shortfalls and interest — though this can be reduced; and

- if choice of fund rules haven’t been followed, choice loadings for the QE day (capped at $1,200 per notice period).

A few other changes worth knowing about

Alongside the core payday superannuation changes, there are a few other updates to be aware of:

- The Small Business Superannuation Clearing House is closing: it currently serves businesses with an aggregated annual turnover of less than $10 million or fewer than 19 employees, but it will close permanently on 1 July 2026. If this affects you, start exploring alternatives sooner rather than later.

- The late payment offset goes away: this offset will only apply to contributions made before 1 July 2026, so you won’t be able to rely on it going forward.

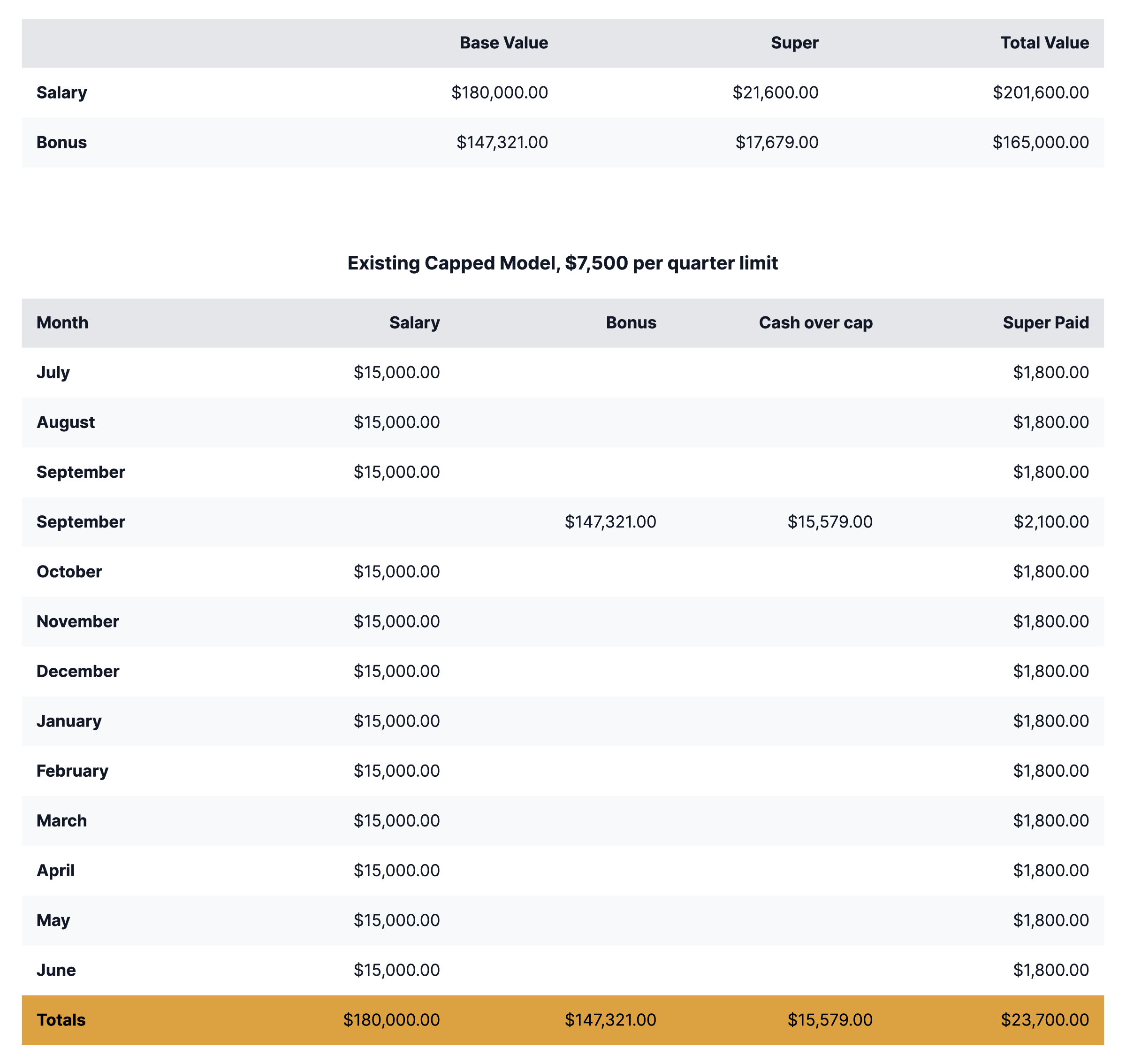

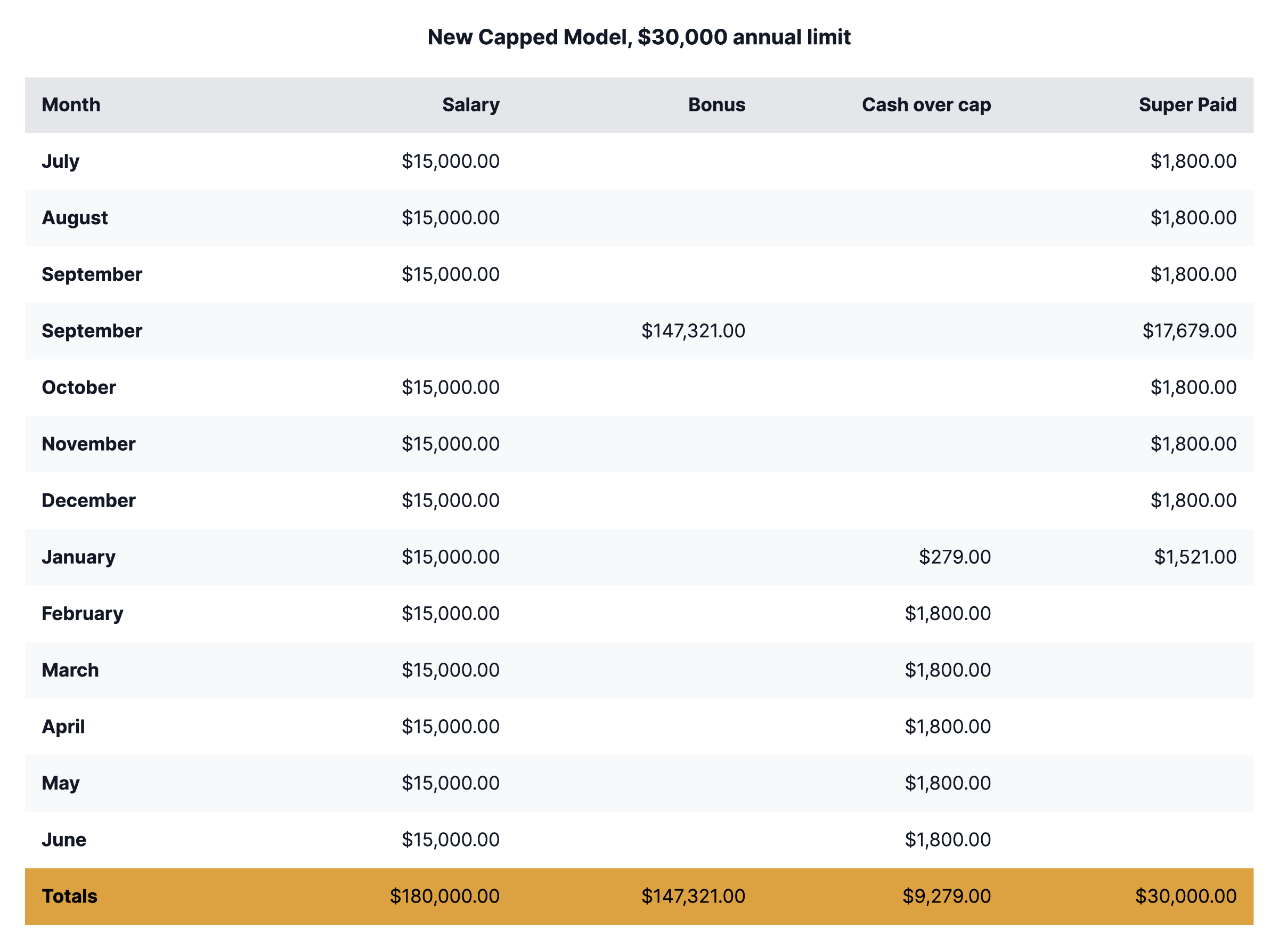

- The maximum contribution base becomes an annual limit: rather than quarterly. One thing to plan for: if you’re currently paying super quarterly and you pay April–June 2026 contributions in July 2026, FY2027 will effectively include 15 months’ worth of contributions rather than 12. It’s worth modelling the cashflow impact of this ahead of time.

See the example below of how the annual limit would impact an employee’s salary and super, based on a total remuneration package value:

Penalties for late payment

If the Superannuation Guarantee Charge isn’t paid within 28 days of becoming payable, the ATO will issue a notice giving the employer a further 28 days to pay.

Miss that second deadline and you’ll face a penalty of 25% of the outstanding amount. That rises to 50% if you’ve received a notice in the preceding 24 months. On the upside, if you pay part or all of the amount before the notice expires, the penalty reduces proportionally.

What the ATO’s compliance approach looks like

The ATO has set out its proposed compliance approach for the first year of the payday superannuation framework in draft Practical Compliance Guideline PCG 2025/D5.

PCG 2025/D5 describes a tiered, risk-based approach. Employers who haven’t paid the minimum required superannuation contributions for their employees are explicitly flagged as high risk.

It’s also worth noting that the guideline only covers the ATO compliance approach until 30 June 2027. By the time it expires, the framework will have been running for nearly a year — so expect the ATO to take a firmer line from 1 July 2027 onwards.

You can read the first-year compliance approach here.

How to get ready

The good news is there’s plenty you can do now to set yourself up well. Here’s where to start:

- Work out how the changes apply to your business. Every situation is a little different, so it’s worth mapping out what needs to change in your own processes.

- Check your payroll systems and employee data are in good shape. Outdated or inaccurate data is one of the most common reasons contributions get rejected, which could trigger an SG shortfall.

- If you use a clearing house, confirm it can distribute contributions to the relevant funds within the seven-business-day window. Not all clearing houses are equal.

- Think about cashflow. Moving from quarterly to payday contributions is a meaningful change for many businesses so model the impact and plan accordingly.

- Talk to your team. Make sure the people responsible for payroll understand what’s changing and when.

- Review your internal policies and governance processes so that any superannuation guarantee contribution issues can be spotted and sorted quickly.

- Check your record-keeping. Make sure you have all the documentation you need for each employee, including choice of fund forms.

If you’re not sure where to start or have questions about how the payday super framework applies to your business, please don’t hesitate to reach out as we’re here to help.

Findex (Aust) Pty Ltd, trading as Crowe Australasia, is a member of Crowe Global, a Swiss verein. Each member firm of Crowe Global is a separate and independent legal entity. Findex (Aust) Pty Ltd and its affiliates are not responsible or liable for any acts or omissions of Crowe Global or any other member of Crowe Global. Crowe Global does not render any professional services and does not have an ownership or partnership interest in Findex (Aust) Pty Ltd.